Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Health insurance is likely one of the top three expenses in your annual budget, sitting right alongside housing and taxes. Whether you are a business owner trying to attract top talent or a freelancer protecting your family, the mechanism you use to secure coverage significantly affects your financial bottom line and your access to medical care. The decision between group health insurance and individual health insurance is not merely a choice between two products; it is a strategic decision about how you prefer to manage risk, taxes, and provider access. Understanding the structural differences between these two distinct markets is essential for securing the best possible value for your healthcare dollar in 2026.

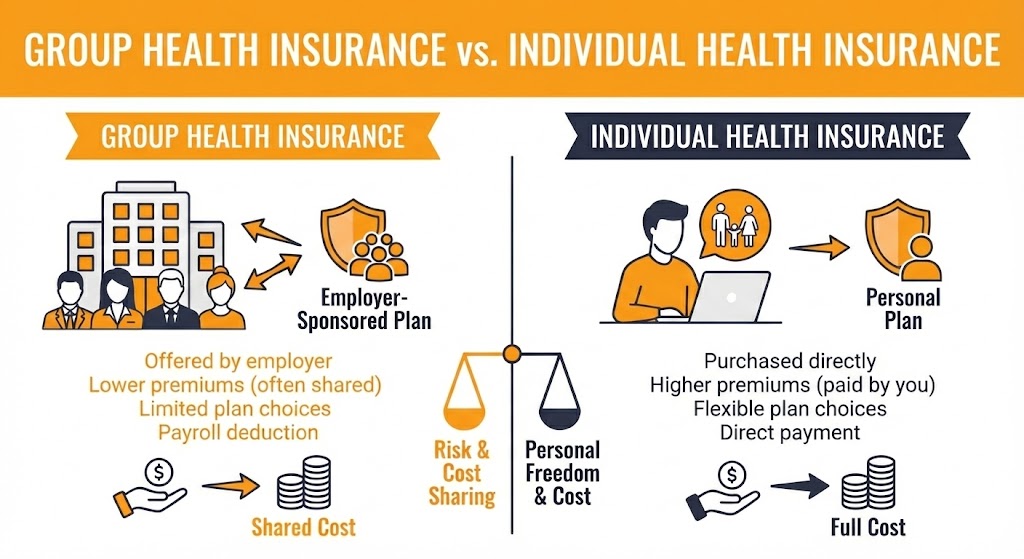

Defining the Core Differences in Coverage Models

The fundamental difference between these two types of insurance lies in who owns the policy and how the risk is distributed. Group health insurance is a single policy issued to an organization, typically an employer, which then covers eligible employees and their dependents. The employer owns the “master policy,” and the employees are effectively certificate holders within that larger contract. This structure allows the insurance carrier to spread the financial risk across a large pool of people. Since the pool includes a mix of young, healthy individuals and older, higher-risk individuals, the premiums tend to be more stable and predictable over time.

In contrast, individual health insurance is a direct contract between a single person (or family) and the insurance carrier. You are the policyholder, and you own the plan entirely. In this market, the risk pool is not limited to a specific company’s workforce but is instead shared across a broad demographic within a geographic region. Because the insurance company cannot rely on an employer to subsidize the cost or enforce participation, individual plans often have higher volatility in premium pricing and may require more active management from the policyholder during annual enrollment periods.

The Financial Impact: Premiums and Tax Advantages

Cost is almost always the deciding factor for both employers and individuals, but the “true cost” of health insurance involves more than just the monthly premium. The tax treatment of these payments plays a massive role in the final calculation.

Pre-Tax vs. Post-Tax Spending

Group health insurance offers a distinct tax advantage that is difficult to replicate in the individual market. When an employer offers a group plan, the portion of the premium paid by the employee is typically deducted from their payroll on a pre-tax basis. This means the money is removed from gross income before federal income tax, Social Security tax, and Medicare tax are calculated. This mechanism effectively lowers the employee’s taxable income, making the insurance “cheaper” than the sticker price suggests. For the employer, every dollar contributed toward employee premiums is fully tax-deductible as a business expense.

Individual health insurance premiums, on the other hand, are generally paid with after-tax dollars. You receive your paycheck, taxes are deducted, and then you pay your insurance bill from your net income. While there are some exceptions—such as self-employed individuals who may deduct premiums or those whose total medical expenses exceed a specific percentage of their adjusted gross income—most people paying for individual coverage do not see an immediate tax benefit. This difference alone can make a group plan significantly more economical for a standard W-2 employee.

Subsidies and the Affordable Care Act

However, the individual market has a powerful equalizer in the form of federal subsidies. The Affordable Care Act (ACA) provides Advanced Premium Tax Credits to eligible households based on income and family size. For lower-to-middle-income families, these subsidies can dramatically reduce the monthly cost of an individual plan, sometimes making it less expensive than the employee contribution required for a group plan. It is important to note that if an employee is offered “affordable” coverage by their employer (as defined by the IRS), they are generally disqualified from receiving these subsidies in the individual market, effectively locking them into the group plan.

Network Access and Provider Choice

Beyond the financials, the ability to see your preferred doctor is the most emotional aspect of health insurance. The structure of provider networks varies significantly between group and individual markets.

The Scope of Group Networks

Group health insurance plans often feature larger, more comprehensive provider networks. Because these plans are sold to diverse employee populations who live in different areas, carriers usually attach their broad PPO (Preferred Provider Organization) or national networks to group policies. This ensures that an employee living in the suburbs and working in the city can both find in-network care easily. For employers, offering a plan with a robust network is a key retention tool, as it minimizes the disruption employees face when seeking medical attention.

The Specificity of Individual Networks

Individual health insurance plans have historically utilized narrower networks to keep premiums competitive. In many ACA marketplace plans, carriers rely heavily on HMO (Health Maintenance Organization) or EPO (Exclusive Provider Organization) networks. These networks often require referrals for specialists and provide no coverage for out-of-network care except in emergencies. While this helps control costs, it requires the consumer to be much more diligent. If you purchase an individual plan, you must verify that your specific doctors and local hospitals participate in that specific plan’s network, as carriers often have different networks for their group and individual products.

Stability, Portability, and Control

The relationship between the insured person and the policy dictates how portable and stable the coverage is. This is often described as the “golden handcuffs” effect of group insurance versus the freedom of individual coverage.

Employment Dependencies

Group health insurance is inherently tied to employment. If you leave your job, are laid off, or retire before age 65, your coverage generally ends on the last day of that month. While federal COBRA laws allow you to continue the coverage for a limited time (usually 18 months), you are required to pay the full premium plus a 2% administrative fee. This sudden jump in cost can be a financial shock. Therefore, group insurance offers excellent stability while you are employed but creates vulnerability during career transitions.

The Freedom of Individual Plans

Individual health insurance offers true portability. Because you own the policy, it is completely decoupled from your employment status. You can switch jobs, start a business, take a sabbatical, or retire early without worrying about losing your health coverage. As long as you continue to pay your premiums, the insurance carrier cannot cancel your policy. This portability is increasingly valuable in the modern gig economy, where workers frequently move between contracts and projects. For those who prioritize autonomy and career flexibility, the individual market provides a safety net that remains constant even when life circumstances change.

Feature Comparison: At a Glance

To summarize the complex distinctions between these two approaches, the following table outlines the operational and financial differences that matter most to consumers and business owners.

| Feature | Group Health Insurance | Individual Health Insurance |

| Policy Ownership | Owned by the Employer (Master Policy). | Owned by the Individual Policyholder. |

| Tax Treatment | Premiums are usually paid Pre-Tax; lowers taxable income. | Premiums are usually paid Post-Tax; limited deductibility. |

| Cost Basis | Rates based on group risk; Employer pays a portion. | Rates based on age/location; You pay 100% (unless subsidized). |

| Network Breadth | Typically, broader PPO networks with national reach. | Often narrower HMO/EPO networks; localized focus. |

| Enrollment | Handled by HR; Guaranteed acceptance. | Self-enrollment; Guaranteed during Open Enrollment. |

| Portability | Not portable; ends when employment ends (COBRA applies). | Fully portable; travels with you regardless of job. |

| Plan Choice | Limited to options selected by the Employer. | Full freedom to choose any carrier/plan in the market. |

The Emerging Hybrid: ICHRA and the Future of Benefits

As we look toward the remainder of the decade, the strict binary choice between group and individual insurance is evolving. A newer model known as the Individual Coverage Health Reimbursement Arrangement (ICHRA) is gaining traction among forward-thinking businesses. This model allows employers to reimburse employees tax-free for their individual health insurance premiums.

This hybrid approach attempts to capture the best of both worlds. It gives employees the freedom to choose their own individual plan—selecting the carrier and network that fits their personal needs—while still receiving a tax-advantaged financial contribution from their employer. For businesses, this removes the administrative burden of managing a group plan and stabilizes their budget, as they can set a fixed monthly allowance for each employee. This trend suggests that while the definitions of group and individual insurance remain distinct, the way they are utilized in the employee benefits landscape is becoming more fluid and personalized.

Choosing the Path That Fits Your Life

Ultimately, the choice between group and individual health insurance depends on your specific position in the market. For established businesses and employees seeking simplicity and lower effective costs, group health insurance remains the gold standard. It offers high-quality coverage with minimal friction and significant tax incentives. However, for entrepreneurs, early retirees, and those who demand total control over their healthcare providers, the individual market offers the necessary freedom and portability to navigate a changing world. At iHealthBrokers, we specialize in analyzing these trade-offs to help you construct a healthcare strategy that protects both your health and your financial future.