Medicare Supplement plans are offered by private insurance companies. They’re meant to help with some of the out-of-pocket health care costs associated with Original Medicare, such as copayments, coinsurance, and deductibles. There are 10 different Medicare supplements—plans A, B, C, D, F, G, K, L, M, and N. Each offers its own variety of benefits at relative costs for personalized coverage.

The reason why Medicare Supplement Insurance (or Medigap) plans cover the many out-of-pocket costs you face with Original Medicare is that, on their own, Parts A and B offer decent, low-cost coverage, but they certainly don’t cover everything.

Besides Medigap, your other additional options include Medicare Advantage and Part D. Unlike Medicare Advantage, which is a full alternative to Original Medicare that includes all of its coverage in a newly structured plan with some additional benefits, supplements are, as the name implies, a “supplement.”

MEDIGAP AND DRUG COVERAGE

Medigap is an addition to coverage options rather than an alternative. This, however, does not mean that you will be paying more—in fact, you will be saving a significant amount on Original Medicare with a supplement plan. Keep in mind though, that you can’t be joined in a Medicare Prescription Drug Coverage plan and have a Medigap policy with drug coverage. This means that if you already have an existent Medigap policy that covers prescription drugs, you’ll need to tell your Medigap insurance company if you join a Medicare Prescription Drug Plan. The Medigap insurance company will then remove the prescription drug coverage from your Medigap policy and adjust your premium.

SAVING MONEY WITH MEDIGAP

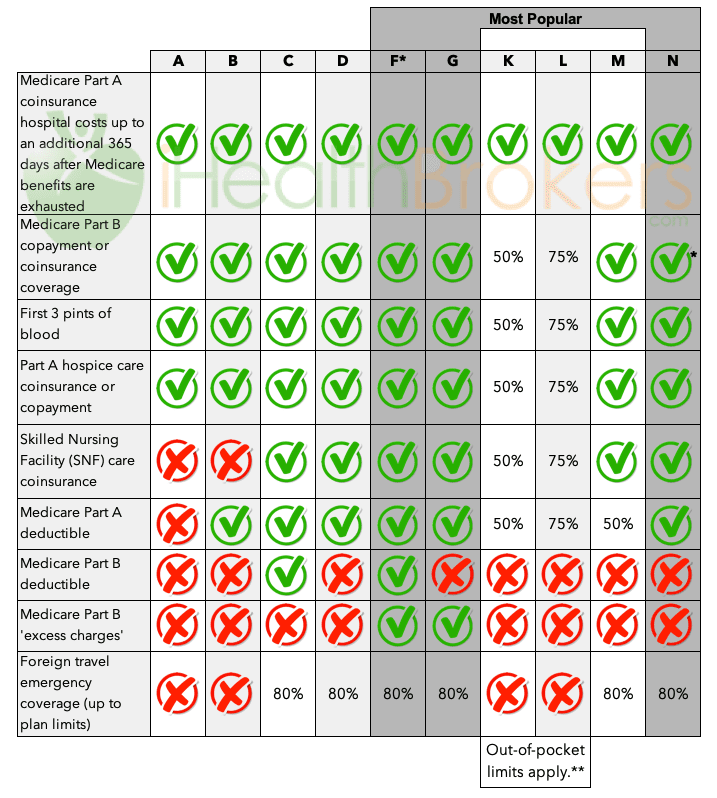

All supplement plans offer this coverage:

Part A Coinsurance & Hospital Costs

Part B Coinsurance or Copayment

First 3 Pints of Blood for Transfusions

Part A Hospice Care Coinsurance or Copayment

The most basic of all the supplement plans is Plan A. All 10 options offer these minimal benefits. The more benefits are added, the more it will cost monthly. However, even as your monthly cost increases, you will still be saving a significant amount on your Original Medicare coverage.

DECIDING ON A SUPPLEMENT PLAN

This is where your decision on a plan becomes important. Yes, you will pay a higher monthly premium for more coverage, but you will also be paying much less out-of-pocket for the healthcare you receive.

Some plans, like Plan K, offer a percentage of benefits to lower your monthly costs:

100% of Part A Coinsurance and Hospital Costs

50% of Part B Coinsurance/Copayment

50% of the First 3 Pints of Blood for Transfusions

50% of Part A Hospice Care Coinsurance or Copayment

50% of Skilled Nursing Care Facility Coinsurance

50% of the Part A Deductible

This way, you know that you are still getting coverage with only half of the total cost coming out of your wallet.

Other plans, like Plan F, offer the fullest possible coverage at a higher monthly cost:

Part A Coinsurance & Hospital Costs

Part B Coinsurance/Copayment

First 3 Pints of Blood for Transfusions

Part A Hospice Care Coinsurance/Copayment

Skilled Nursing Care Facility Coinsurance

Part A Deductible

Part B Deductible

Part B Excess Charges

80% of Foreign Travel Emergency Care

Keep in mind that Medicare Plan F is not available anymore to some extent. Due to a change in federal law, people who have become eligible for Medicare after December 31, 2019. do not qualify for Plan F. However, Plan F continues to be available to everyone who became eligible for Medicare before that date.

No matter which one of the plans you choose to enroll in, you will save a lot of money on your Original Medicare coverage. Check out our Medicare Supplement Plan Comparison to review your full options and choose a supplement that works best for you.

ENROLLING IN A SUPPLEMENT PLAN

If you have chosen a supplement plan, your next step is to enroll. The best time to do so is during your Medigap General Enrollment Period (GEP).

During the 7 months following your 65th birthday, you can enroll in any Medigap plan without fear of being turned away due to your health. After the General Enrollment Period, it may be harder to enroll but still possible in case you have a medical condition.

Another option you have is to simply enroll during your Medigap Open Enrollment Period. It is during this time that you can buy any Medigap policy sold in your state, even if you have health problems, and will generally get better prices and more choices among policies. This period automatically starts the first month you get your Medicare Part B (Medical Insurance) and you’re 65 years old or older. This time period can’t be changed or repeated and after the period ends, you may not be able to buy a Medigap policy. If you’re able to buy one, it may cost more due to past or present health problems.

Taking all this into consideration, we typically advise that you enroll in one as soon as you are able.