Overwhelmed with health insurance jargon? Let’s go over some of the basic terms to help you understand how health insurance works video.

Premium

First let’s talk about monthly premiums. This is fairly easy to understand. Your monthly premium is the amount you pay monthly to keep your insurance active. If you don’t pay your monthly premium, you won’t have insurance.

You cannot judge a plan based on premiums alone! A low monthly premium doesn’t necessarily mean a bad plan, just like a higher monthly premiums doesn’t necessarily mean a good plan.

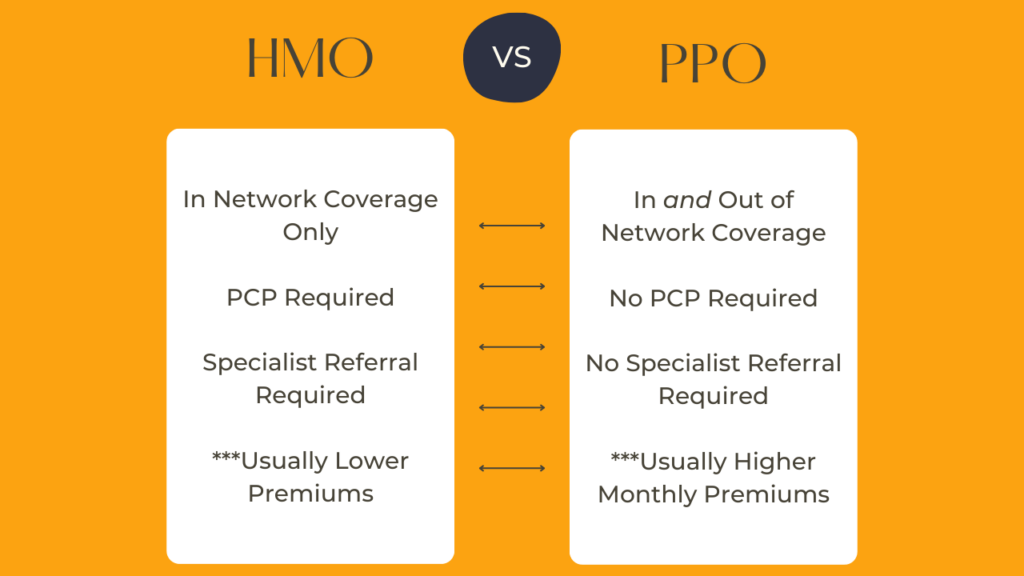

Generally PPOs will have higher monthly premiums and HMOs will have lower monthly premiums.

You may also be eligible for a premium tax credit if you purchase a plan through the marketplace.

A premium tax credit is just a tax credit paid upfront and it is reflected in a discounted monthly premium. You may be eligible for a premium tax credit based on your income and household size. You will find out if you are eligible for a premium tax credit by answering a few simple questions on healthcare.gov

Deductible

The next financial term to understand is your deductible. This is the amount that you must meet out of pocket (or at full cost) before your insurance begins to contribute to the cost share.

You should know that very often plans with higher deductibles have lower premiums and vice versa. There is usually an inverse relationship.

Usually there are many services covered prior to meeting your deductible, for example basic doctors visits, urgent care, prescriptions, etc… Often the deductible is really applied for procedures in an inpatient or outpatient setting.

Not only are many services covered even prior to meeting your deductible, some have no charge (usually preventative and wellness services). Also, group health insurance and marketplace plans must offer at least the 10 essential benefits.

Copays/Coinsurance

When you use your insurance you will likely have to pay a copay or coinsurance

A copay is a fixed amount. For example, you might have a copay of $25 to see your doctor, $50 for the urgent care and $250 for the ER.

Coinsurance is a variable amount. It is a percentage of the cost. So, using our example above, you might have a 25% coinsurance for inpatient care. So, your bill is determined by the cost of the service.

If you’ve seen the metal tiers on the marketplace, these metal tiers really indicate the cost sharing or coinsurance structure.

Out of Pocket Maximum

Finally, another term and number to be familiar with is the out of pocket maximum. This is the maximum that you can be billed in a plan’s year.

In 2024, the maximum OOP max are $9,450 for an individual and $18,900 for a family.

Now of course, you are much likelier to find these higher OOP max in a HDHP or catastrophic coverage plans. Usually OOP Max’s will be much lower, especially if you have employer sponsored group health coverage.

Basically, if you have extensive medical needs in a given year, your insurance plan will step in to protect you from major medical bills. If you hit for OOP Max, your plan will take on the bills for the remaining plan year for any covered in network services.

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.