Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

If you don’t receive health insurance through your employer or are self employed, how are you supposed to save money on medical expenses? There are several options available.

SHOP

SHOP stands for small business health options programs. If you are a small business owner with less than 50 FTE, you may be able to offer these plans to your employees.

Employers with more than 50 full time employees are required to provide health insurance. If you have less than 50 full time employees you may wish to do so anyway. A recent study indicated that 56 percent of U.S. adults with employer-sponsored health benefits said that whether or not they like their health coverage is a key factor in deciding to stay at their current job. And 46 percent said health insurance was either the deciding factor or a positive influence in choosing their current job.

So, if you wish to attract top talent, you may wish to consider health insurance. (Even if you are not legally obligated to do so)

If you’d like to learn more about your state’s regulations, visit your state’s individual website or marketplace. Healthcare.gov can also redirect you to your state’s marketplace if you are unsure.

In order to be eligible for the SHOP, you must have between 1-50 full time employees. At least one of these employees cannot be a business owner or partner or spouse of the business owner or partner. Additionally at least 70% of your employees must elect to take part in the program.

Marketplace

If you are the sole employee of your business or you are not in the financial position to offer plans through SHOP, you may want to consider a regular marketplace place.

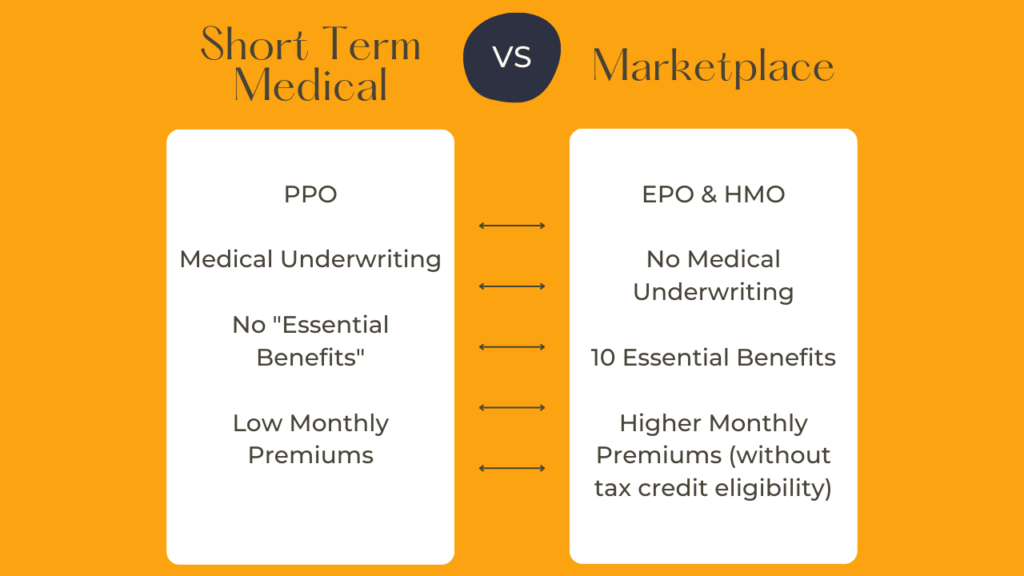

Marketplace plans must all offer at least the 10 essential benefits. You cannot be denied or charge more based on a preexisting condition.

Your monthly premium is largely determined by your eligibility for a premium tax credit. Eligibility is determined by your income and household size. Premium tax credits can save you quite literally thousands of dollars per year.

Healthcare.gov will determine you eligibility by having you answer a few simple questions.

Often, it may be difficult to estimate next year’s income if you are self employed. This is often the case if you are in the beginning stages of your career.

However, it is important to estimate as accurately as possible. If you over estimate, you’ll likely just receive a larger tax refund when you file your taxes. But if you underestimate, you may need to pay a portion or possibly all of that premium tax credit back.

This is why we highly recommend working with an experienced account tax professional.

HSA

If you are looking to lower your MAGI, you may want to consider a HDHP which offers an HSA.

HSAs are health savings accounts The amount that you contribute is pre-tax. This can your taxable income. If you are on the brink of being eligible for a premium tax credit, this could possibly push you over the edge. You could save you thousands of dollars per year.

HSAs are interest bearing accounts where your money is held. The interest is not taxed. You can use the money in these accounts for qualified medical expenses or simply let it sit there. It is your money.

You can even invest a certain portion of it and money from those investments is also not taxable. If you hold onto this account until you retire, you can use it as a basic retirement account.

Short Term Medical

If you are ineligible for a premium tax credit through the marketplace, you may want to look into a short term medical plan. These are a type private insurance plan that is offered for a period of up to three years in most states.

There are other options as well such as catastrophic coverage plans, critical illness plans and hospital indemnity plans.