Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Health Insurance is undeniably important but it can be expensive! Here are some health insurance savings hacks that can definitely help you save money.

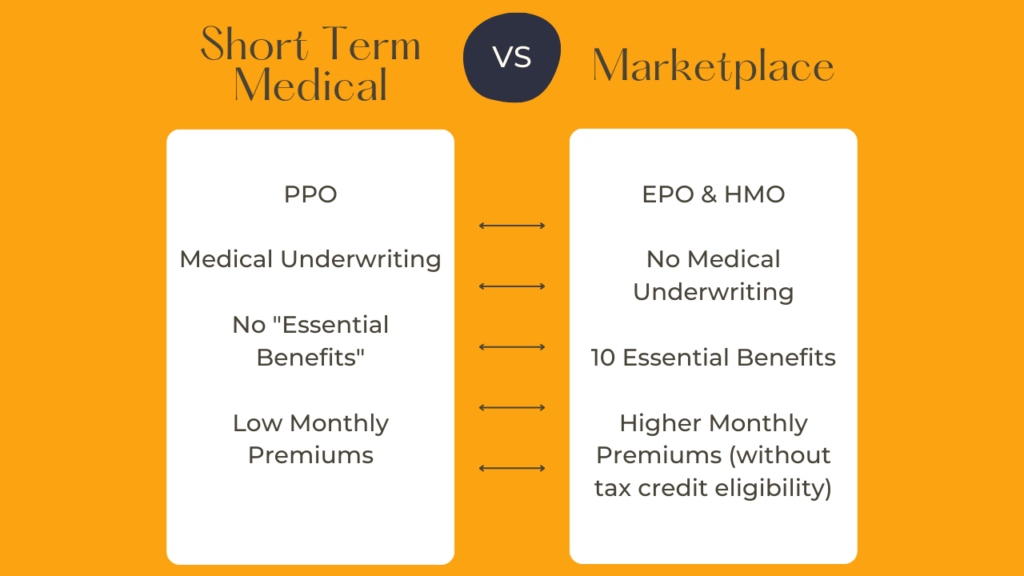

Marketplace Plans

You’ll sometimes hear plans on the marketplace referred to as obamacare. These plans are part of the affordable care act. All plans must offer the 10 essential benefits. However, plans can choose to offer better benefits. You cannot be charged more or denied based on pre-existing conditions

MAGI

Your eligibility for a premium tax credit (discounted monthly premium) is determined by your household size and MAGI. Your MAGI is your modified adjusted gross income.

For most people your MAGI is the same as your AGI although there are a few exceptions. We recommend working with an accountant or certified financial expert to maximize any deductions you may be eligible for. Lowering your MAGI could save you thousands of dollars per year.

You could also enroll in an HDHP and contribute to an HSA to lower your MAGI.

Silver Plan

Although Bronze plans tend to have the lower monthly premiums, a silver plan may actually offer you the best savings!

If you are eligible for a premium tax credit, you may be eligible for extra savings with a silver plan. If this is the case, pay special attention to the silver plans when comparing!

Pick the Right Plan

A commonly overlooked savings hack is to pick the right plan. You cannot judge a plan based on premium alone. For example, a less expensive plan may end up costing you if none of your doctors or hospitals are in network.

A higher premium plan may end up saving you money if you have more extensive medical needs and this plan offers a lower deductible or OOP MAX.

Work with a broker to make sure you are getting the best bang for your buck.

Short Term Medical Plans

If a marketplace plan isn’t for you either because you are ineligible for a premium tax or you need the flexibility that comes with a nationwide PPO plan, look into a STM. They may offer you a great savings!

Catastrophic Coverage

In the past, STM were referred to as catastrophic coverage plans because they offered such bare bones coverage. That’s really not the case any more because so many plans offer such extensive benefits. However catastrophic coverage plans are still available and may be a great way to have access to a lower cost healthcare plan. They are another types of HDHP with a lower monthly premium.

Catastrophic plans on the marketplace will still offer some benefits prior to meeting your deductible. For example, you will have 3 primary care doctor visits per year covered even if you haven’t met your deductible yet.

Other than that, your insurance will mostly be there for large medical expenses. You likely will not have any coverage until your’ve met not only your deductible, but your out of pocket maximum.

Out of Pocket Maximum

Your OOP is the maximum amount that you can be charged for medical spending in a given year. Once you’ve met your OOP max, your insurance carrier will take on teh remainder for any covered, in network benefits.

So, with a catastrophic coverage plan, you could pay a low monthly premium and have access to a few basic doctor’s visits. For anything relatively minor like prescriptions, a trip to the urgent care or even the ER, you would likely have to pay out of pocket. But, if you have a major medical bill for something such as surgery, you would only have to pay the out of pocket maximum and your insurance would pay the rest.

In 2024, the maximum out of pocket max for a marketplace plan is $9,450 for an individual and $18,900 for a family.

HSA & HDHP

We’ve already touched on this briefly when discussing marketplace but let’s discuss HDHPs and HSAs a little bit more in depth.

HDHPs are high deductible health plans. Some offer a special benefit called an HSA- health savings account. HSAs are only offered with HDHPs.

Every year the IRS sets the minimum deductible for what can be considered a HDHP. In 2024, the minimum deductible to be considered an HDHP is $1600 for an individual and $3200 for a family plan.

If you enroll in an HDHP, some services such as preventative care and wellness visits will be covered even prior to meeting your deductible.

HSA

If your HDHP offers an HSA, this is a great money savings hack.

HSAs are health savings accounts. You can contribute up to a certain amount and that amount is pretax. Basically this will lower your taxable income. This can possibly put you into a lower tax bracket to save money when you file or even make you eligible for a larger premium tax credit if you enroll in a plan through the marketplace.

Every year the IRS set a maximum amount that you can contribute. In 2024 that amount is $4150 for an individual or $8300 for a family.

The money that you contribute will sit in an interest bearing account. That interest is also not taxed. You can withdraw the funds for a qualified medical expense and the list is very long even including chiropractic care, dental bills or even OTC medications.

But you don’t have to use those funds. You can let them sit there and continue to accrue interest. The account will roll over from year to year. You can even invest a certain portion of it. Anything earned from those investments will also be tax free.

Until you turn 65, there is no penalty for withdrawing for a qualified medical expense. After 65, it converts to a basic retirement account and you can use it as you see fit.