Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Date Released by CMS: 2016-05-06

Title: Special Enrollment Period Health Insurance Marketplace

Contact: press@cms.hhs.gov

Special Enrollment Period Health Insurance Marketplace and the Consumer Operated and Oriented Plan Program

HHS is taking new steps to strengthen the integrity of special enrollment periods (SEPs) and to simplify rules for the Consumer Operated and Oriented Plan (CO-OP) program to allow them to more easily raise capital. These changes were instituted in order to improve stability in the Health Insurance marketplace and help consumers’ access to quality, affordable coverage.

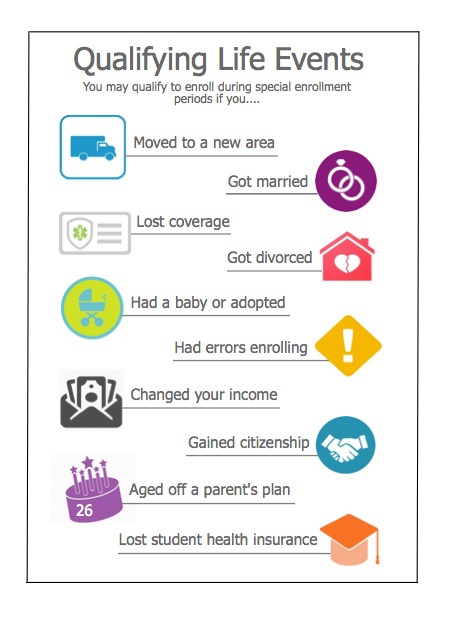

Special Enrollment Periods

While SEPs provide a critical pathway to coverage for qualified individuals who experience qualifying events and need to enroll in or change qualified health plans (QHPs) outside of the annual open enrollment period, it’s equally important to avoid SEPs being misused or abused. As it announced today, HHS is tightening the rules for certain special enrollment periods and making clear that SEPs are only available in six defined and limited types of circumstances.

New rules limit the circumstances in which someone may qualify for the permanent move SEP to ensure consistency with the original purpose of that SEP. An Interim Final Rule with Comment (IFC) published in the Federal Register provides that individuals requesting a “permanent move” SEP must have minimum essential coverage for one or more days in the 60 days preceding the permanent move, unless they were living outside of the United States or in a United State territory prior to the permanent move. This ensures that individuals are not moving for the sole purpose of obtaining health coverage outside of the open enrollment period.

We are also making conforming changes to ensure that individuals who were incarcerated, or were previously in the coverage gap in a non-Medicaid expansion state and have moved and become newly eligible for advance payments of the premium tax credit (both of whom would previously have qualified for the permanent move SEP) may continue to qualify for a special enrollment period. Because these individuals were previously unable to have minimum essential coverage or exempt from having minimum essential coverage prior to the qualifying event that qualifies them for this SEP, we are not requiring that they had prior minimum essential coverage to qualify for an SEP.

The IFC also removes a January 1, 2017 implementation deadline by which Marketplaces would otherwise have had to provide advance availability of the permanent move SEP and provide a SEP for loss of a dependent, or for no longer being considered a dependent due to divorce, legal separation, or death. Marketplaces can still provide either SEP, but implementation and the timing of that implementation are at the option of the Marketplace.

Finally, clarified in separate guidance that SEPs are only available in six defined and limited types of circumstances: (1) losing other qualifying coverage, (2) changes in household size like marriage or birth, (3) changes in residence, with significant limitations, (4) changes in eligibility for financial help, with significant limitations, (5) defined types of errors made by Marketplaces or plans, and (6) other specific cases like cycling between Medicaid and the Marketplace or leaving Americorps coverage.

CO-OP Program

The IFC also makes several changes to the regulations governing the CO-OP program that are intended to enhance the ability of CO-OPs to attract investors and develop new relationships that we anticipate will support their short and long-term financial viability. These changes enhance the ability of CO-OPs to enter into new affiliations or capital transactions with other entities in a manner common in the private sector, while preserving the fundamental member-governed nature of the CO-OPs. We encourage CO-OPs to actively consider seeking additional sources of funding as they plan for the year ahead.

The IFC removes the requirement that a majority of voting directors be members of the CO-OP, and that all directors be elected by a vote of CO-OP members. However, a majority of directors must still be elected by the members of the CO-OP. This adds flexibility to board eligibility, consistent with private sector practices, and removes a potential barrier to private sector investments, while preserving the fundamental member-governed nature of the CO-OPs.

The IFC also provides clarity regarding compliance with the requirement that at least two thirds of the plans issued by a CO-OP be QHPs in the individual or small group market. The rule clarifies that, if a CO-OP temporarily fails to meet the standard in a given year, HHS would not necessarily require early loan repayment as long as the CO-OP is in compliance with any applicable requirement to offer silver and gold plans, has a specific plan and timetable to meet the two-thirds requirement, and acts with demonstrable diligence and good faith to meet the standard. A CO-OP must ultimately come back into compliance with the two-thirds standard in future years.

Finally, the IFC provides clarity relating to the prohibition on a CO-OP converting or selling to a for-profit or non‑consumer operated entity. The question has arisen as to whether the sale or conversion of policies to a non-CO-OP issuer in connection with the wind-down of a CO- OP is prohibited. If a CO-OP is out of compliance with this provision, the CO-OP will cease to be a qualified non-profit health insurance issuer, and certain rights under the CO-OP Loan Agreement will become available to CMS, including the right to accelerate repayment of the loans or terminate the Loan Agreement itself. However, in the appropriate circumstances, to preserve coverage for enrollees upon insolvency of the issuer, notwithstanding those remedies, HHS recognizes that a CO-OP could elect to enter into such a transaction. Any sale, conversion, or other change to contract terms with cost implications to the government would be reviewed by CMS prior to implementation.