Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

ACA (Obamacare) Healthcare Open Enrollment 2024 runs from 11/01/2024 through 01/15/2025. During this time, you can enroll in ACA-compliant plans for coverage beginning on 01/01/2025. For applicants applying after 12/15/2024, coverage will begin on 02/01/25.

There have been a number of changes for 2024 healthcare plans including expansion from some of the biggest ACA carriers into new states and markets. In addition, renewal increases are down significantly which is great!

2022 Health Plan Guide

Our Healthcare Open Enrollment 2024 Health Plan Guide will help you navigate newly available plans compared to traditional ACA plans.

National PPO Plan Options

Many carriers are now offering non-ACA PPO plans. These plans have much lower rates than traditional ACA plans and can be renewed for up to 3 years before having to purchase a new plan. The Healthcare Open Enrollment 2024 Plan Guide above will allow you to quote these plans. Be aware that not all carriers allow their rates to be shown online, so for the most accurate comparison, give us a call at (888) 918-0518.

Ambetter Expansion

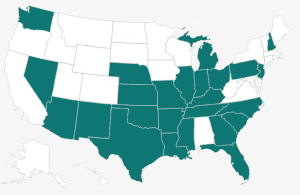

Ambetter has expanded and is now in the 25 states below for Healthcare Open Enrollment 2024. Ambetter is the low-cost leader in most states and also has been very dominant with their Silver plans with cost-sharing reductions. Ambetter has been expanding aggressively since the inception of the ACA and is one of the few carriers who seem to have figured out how to thrive in an ACA world.

- Arizona

- Arkansas

Florida

Florida- Georgia

- Illinois

- Indiana

- Kansas

- Kentucky

- Louisiana

- Michigan

- Mississippi

- Missouri

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- North Carolina

- Ohio Oklahoma

- Pennsylvania

- South Carolina

- Tennessee

- Texas

- Washington

Bright HealthCare Expansion

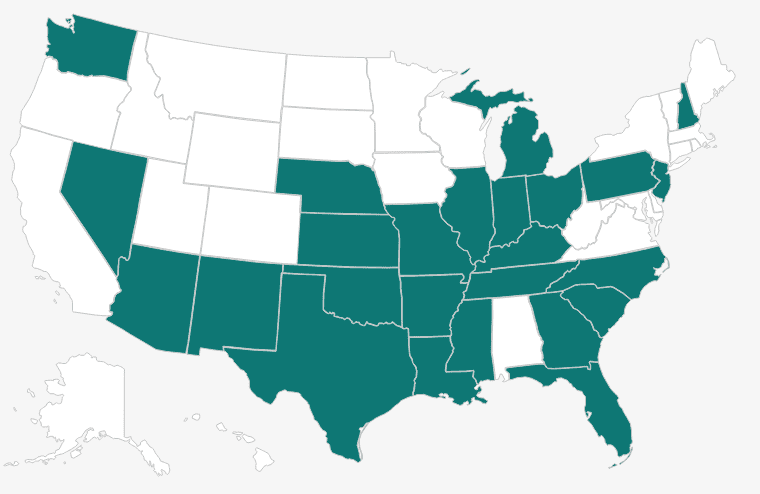

Bright HealthCare is another company that is starting to flourish within the ACA. Bright HealthCare Expands Affordable Plans in 42 New Markets for 2024 Including Texas, Georgia, Utah, and Virginia.

They have expanded into the states below. This is huge news as some of these markets only had 1 insurer as of 2018 for individual and family health plans.

Oscar Expansion

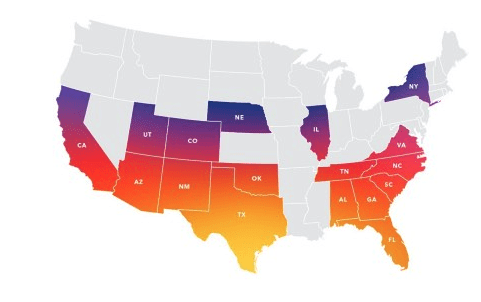

Closing out our list of carriers making big waves for Healthcare Open Enrollment 2024 is Oscar and this list isn’t necessarily in order. Oscar now has health plans for individuals available in 18 states. Oscar came about, also with the ACA to try and reinvent healthcare and so far, they are succeeding. According to a recent survey, 90% of Oscar members say that Oscar saves them time and money compared to other insurers. Their Net Promoter Score which is a measure of customer satisfaction comes in at 66, over 3 times the industry average.

Closing out our list of carriers making big waves for Healthcare Open Enrollment 2024 is Oscar and this list isn’t necessarily in order. Oscar now has health plans for individuals available in 18 states. Oscar came about, also with the ACA to try and reinvent healthcare and so far, they are succeeding. According to a recent survey, 90% of Oscar members say that Oscar saves them time and money compared to other insurers. Their Net Promoter Score which is a measure of customer satisfaction comes in at 66, over 3 times the industry average.