Medigap plan M: Overview

Medicare supplement insurance plans, widely known as Medigap plans, are an essential consideration for beneficiaries seeking to manage the out-of-pocket expenses associated with Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). While Original Medicare provides fundamental coverage, it does not cover all medical costs, famously leaving beneficiaries responsible for approximately of approved services, along with various deductibles and copayments, which are known as the “gaps” in coverage. Medigap policies are private health insurance plans specifically designed to step in and pay these remaining costs, effectively filling the financial “gaps” in Original Medicare. These plans offer beneficiaries the significant advantage of being able to visit any doctor or facility across the country that accepts Medicare, and they introduce predictability to healthcare budgeting. Since the benefits are standardized by the government, the core coverage of a Medigap Plan M is identical, regardless of the private insurance company that sells the policy. Among the ten standardized options, Medigap Plan M is structured to appeal specifically to beneficiaries seeking a favorable balance between comprehensive protection and a lower monthly premium.

Understanding Medigap Plan M Coverage and Benefits

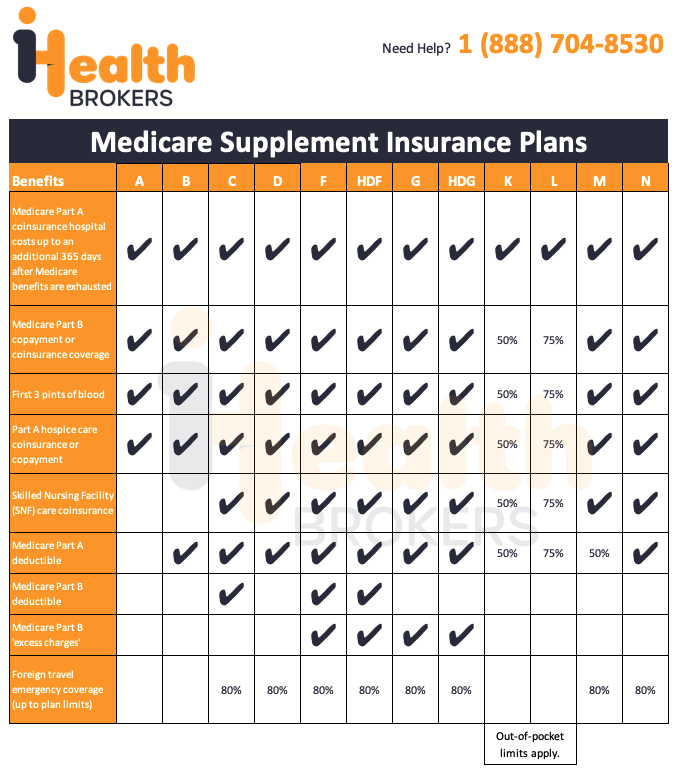

Medigap Plan M provides a substantial level of coverage designed to significantly reduce the financial exposure of Medicare beneficiaries. A primary benefit of this plan is its commitment to covering of the coinsurance and copayments for services covered by Medicare Part B once the beneficiary has satisfied the annual Part B deductible. This comprehensive approach to outpatient costs means that once the annual deductible is met, the plan fully covers a wide range of services, including doctor visits and medical procedures, which is a major financial safeguard.

The key feature distinguishing Medigap Plan M is its cost-sharing provision for the Medicare Part A deductible. Plan M covers 50% of Medicare Part A’s deductible for inpatient hospital stays. This calculated sharing of the Part A deductible is precisely what allows Plan M to offer a generally lower monthly premium compared to plans that cover the deductible in full, making it a smart option for budget-conscious individuals who prefer to manage a single, moderate deductible in the event of a hospital stay.

Furthermore, Plan M ensures a high degree of protection for other medical expenses. It fully covers the Medicare Part A hospital coinsurance and hospital costs for up to an additional 365 days after Original Medicare benefits are exhausted. The plan also takes care of the costs associated with Part A hospice care coinsurance and copayments, as well as skilled nursing facility care coinsurance. For medical procedures, Plan M covers the cost of the first three pints of blood, and it extends its protective features to travelers by covering 80% of approved costs for foreign travel emergency care, subject to the plan’s limits.

Medigap Plan M Exclusions and Cost Savings

To maintain its competitive and often lower monthly premiums, Medigap Plan M strategically omits coverage for two specific costs. Importantly, the plan does not cover the Medicare Part B deductible, meaning the beneficiary is responsible for this annual outpatient cost before the plan’s coverage for Part B coinsurance takes effect. Additionally, Plan M does not cover Medicare Part B excess charges, which are the modest, optional fees providers can charge above the Medicare-approved amount if they do not accept Medicare assignment. By having beneficiaries assume responsibility for these two specific costs, the insurance carrier can significantly reduce the plan’s overall risk, resulting in a more affordable supplement plan’s monthly premium. This structure makes Plan M an ideal fit for those willing to accept predictable out-of-pocket expenses in exchange for lower ongoing premiums.

Popularity of Medigap Plan M in the Current Market

Medigap Plan M occupies a niche in the Medicare Supplement market, appealing strongly to a specific segment of beneficiaries. While popular choices like Plan G and Plan N, which offer broader initial coverage, generally see higher enrollment numbers, Plan M provides a compelling alternative for the value-seeker. The plan is a prudent selection for those who are healthy, infrequently hospitalized, and focused on securing a lower monthly rate while retaining comprehensive coverage against the potentially high cost of Part B coinsurance. Its distinct cost-sharing model for the Part A deductible serves as a key differentiator, appealing to beneficiaries who are comfortable with calculated self-insurance against specific, less frequent costs in favor of guaranteed savings on their ongoing premiums.

Enrollment in Medigap Plan M: Timing is Key

Any individual enrolled in both Medicare Part A and/or Part B is eligible to enroll in Plan M. The most opportune time to secure coverage is during the beneficiary’s six-month Medigap Open Enrollment Period (OEP), which begins on the first day of the month they turn 65 and are enrolled in Medicare Part B. During this vital window, federal law guarantees the right to purchase Plan M without any medical underwriting, protecting beneficiaries from being denied coverage or charged a higher premium due to pre-existing conditions. Enrollment outside of this six-month period may subject the application to medical underwriting, emphasizing the critical importance of acting within the OEP to ensure access to the best available rates and guaranteed coverage for Medigap Plan M.

Medicare Plan M in 2025

For the year 2025, the essential benefits and structure of Medigap Plan M are anticipated to remain unchanged, as Medigap policies are standardized by federal regulation. The plan will continue to serve as a cost-sharing model, covering 50% of the Part A deductible and 100% of Part B coinsurance after the deductible is satisfied. While the core benefits are fixed, it is important to recognize that the specific dollar amounts for the Medicare Part A and Part B deductibles are adjusted annually by the Centers for Medicare and Medicaid Services, which will directly influence the beneficiary’s out-of-pocket expenses for 2025. Therefore, while the coverage remains reliable, beneficiaries should review the newly announced deductible figures and compare the updated premium rates for Plan M offered by various insurance carriers, which are subject to fluctuation based on market trends and pricing strategies.

Questions and Answers on Medigap Plan M

1. What percentage of the Medicare Part A deductible does Medigap Plan M cover? Medigap Plan M covers 50% of Medicare Part A’s deductible for inpatient hospital stays.

2. What are the two specific costs that Medigap Plan M does not cover? The two specific costs that Medigap Plan M does not cover are the Medicare Part B deductible and Medicare Part B excess charges.

3. What does Plan M cover for Medicare Part B services after the deductible is met? After the annual Part B deductible is satisfied, Plan M covers 100% of the coinsurance and copayments for services covered by Medicare Part B.

4. What advantage does the cost-sharing structure of Plan M offer to the beneficiary? The cost-sharing structure, particularly only covering of the Part A deductible, allows Plan M to offer a generally lower monthly premium compared to more comprehensive plans.

5. When is the best time for an eligible individual to enroll in Medigap Plan M without medical underwriting? The best time to enroll is during the six-month Medigap Open Enrollment Period, which starts on the first day of the month the individual turns 65 and is enrolled in Medicare Part B.

Read more on Medicare Plan M here:

BEST Medicare Supplement Plans for 2025 Explained!

FOOTNOTES:

1. HDF and HDG are deductible versions of the F and G, respectively. If you choose one of these options, this means that you must pay for Medicare-covered costs up to the deductible amount of $2,490 (2022) before your Medigap plan pays anything.

2. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 copayment for emergency room visits that don’t result in an inpatient admission.

3. Plan F, High Deductible Plan F (HDF) & Plan C are ONLY available to those who were considered Medicare-eligible prior to 2020.

4. Out-of-pocket limits for Plan K are $6,620 (2022) and $3,310 (2022).