Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

How do your retirement savings stack up to the national average? Do you have enough saved to retire early or even retire comfortably at age 65? Let’s go over some retirement basics and discuss social security, medicare and even a health insurance savings hack to help boost your retirement account.

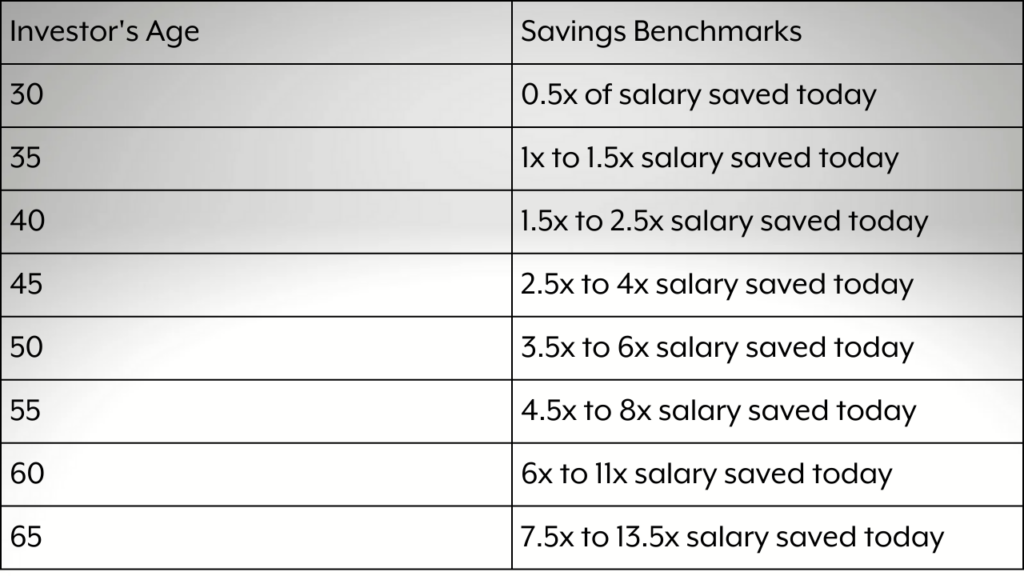

Retirement Savings

First let’s start with retirement savings. Let’s talk about the average retirement savings by age.

These numbers are a little concerning considering how much it is recommended you have to live comfortably in retirement.

Social Security

It’s become obvious that social security alone isn’t enough for most Americans to retire on.

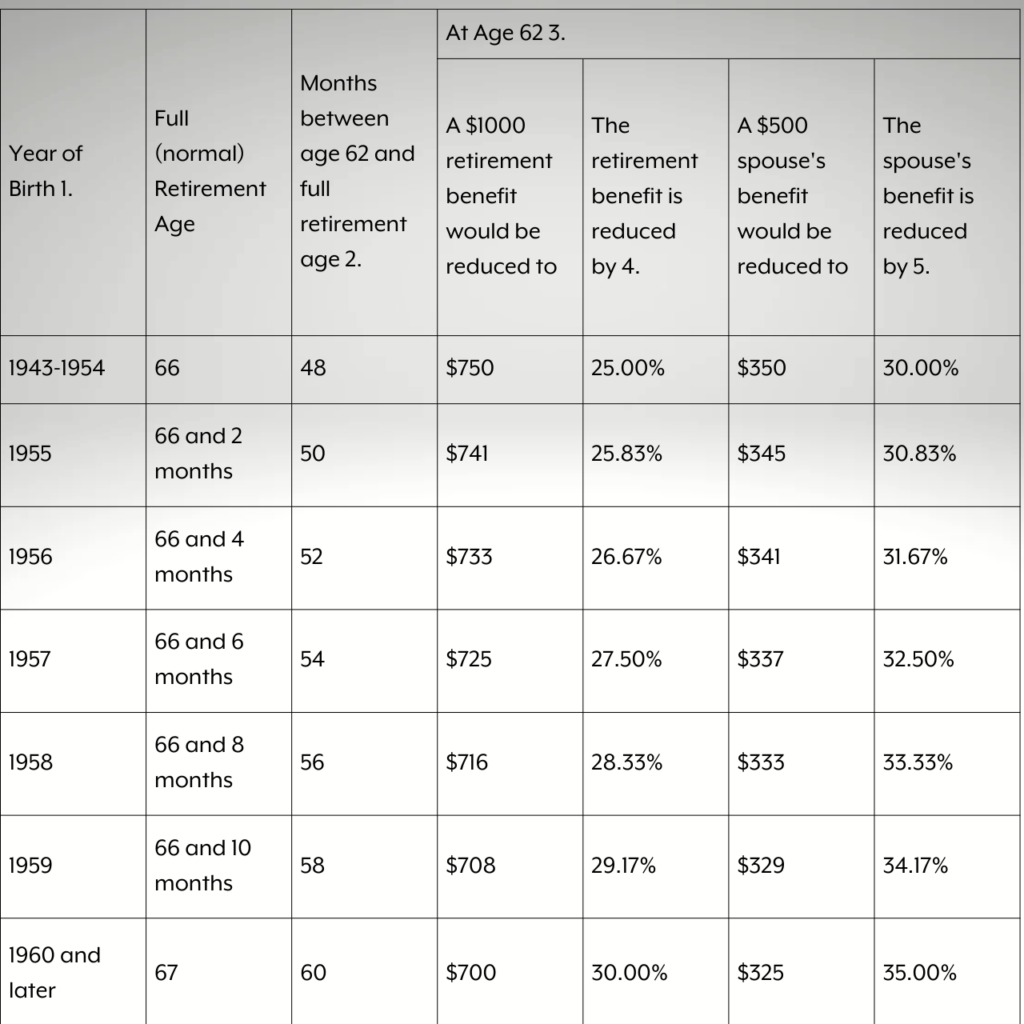

The minimum age to claim benefits is 62.1 If you are turning 62 and need the income from Social Security to support yourself, you can start claiming your benefits now.

However, if you have enough other income to keep you going until you are older, you may want to delay and increase the size of your benefit.

FRA

The size of your monthly Social Security benefit depends on several factors:

- How much you earned over the years

- Your Birth Year

- Your age when you started claiming (even down to the month)

You’ll receive your full monthly benefit if you start claiming when you reach what Social Security considers your FRA which is your full retirement age. Initially, the FRA was 65 when Social Security first began. However, it has recently been raised to 67 for anyone born in 1960 or later.

Now that you understand your FRA, you also need to understand how retiring at different ages affects your benefits.

Remember, you can claim social security benefits prior to reaching your FRA. However, you will receive a smaller payment. And those benefits will not increase once you reach your FRA, you will have a smaller payment for the rest of your life. These numbers may become important when calculating your Medicare payment. We’ll discuss that later in the video.

Similarly, if you wait until after your FRA, you will receive a larger payment. This goes up until age 70, so no need to wait longer than that.

HSA Investments

So, even with social security, you’re probably looking at other ways to bolster your retirement account.

You may want to consider investing in an HSA.

An HSA is a health savings account. It is your account with your money in it. The money that you contribute to your HSA is pretax. This can lower your taxable income and therefore make you eligible for lower taxes. So either a larger refund or a smaller amount owed.

Every year, the IRS sets the maximums that you can contribute to your HSA depending upon whether you contribute as an individual or a family.

HSAs offer what’s known as a triple tax advantage. We’ve already covered one of the three tax advantages which is that your contributions are pretax therefore lowering your taxable income.

As stated, an HSA is just a type of bank account. However, these accounts are interest bearing. The interest accrued by your account is also not taxable.

And number three of the triple tax advantage is that as long as you use the funds for qualified medical expenses, the money you withdraw will not be taxed or penalized.

If you max out on your HSA contribution and invest wisely, it is likely you could achieve a very large retirement fund.

If you are using your HSA really as a wealth building tool, you don’t have to pull money from it to pay for medical expenses. Instead, let it roll over from year to year. Invest wisely and let that interest accrue. That money will be waiting there for you when you turn 65 because at that point the account will convert to a basic retirement account.

And if you are lucky enough to retire early, you can let it continue to grow or use it for medical expenses.

Medicare Basics

You’ll first become eligible for Medicare when you turn 65. However, if you are working past the age of 65 and maintaining creditable coverage, you may want to defer Medicare. Follow the instructions on the back of the card and send it back. If you keep the card, you keep Medicare Part B and you will be charged for it.

When you do retire (age 65 or beyond), your Part B premium is determined by your income. However, Medicare is looking at your income from two years prior. So, if you are now making less money (and you likely are), it is advised that you file IRMAA.

This form may help to remove an additional adjustment that Medicare wants you to pay which can lower your monthly premiums.

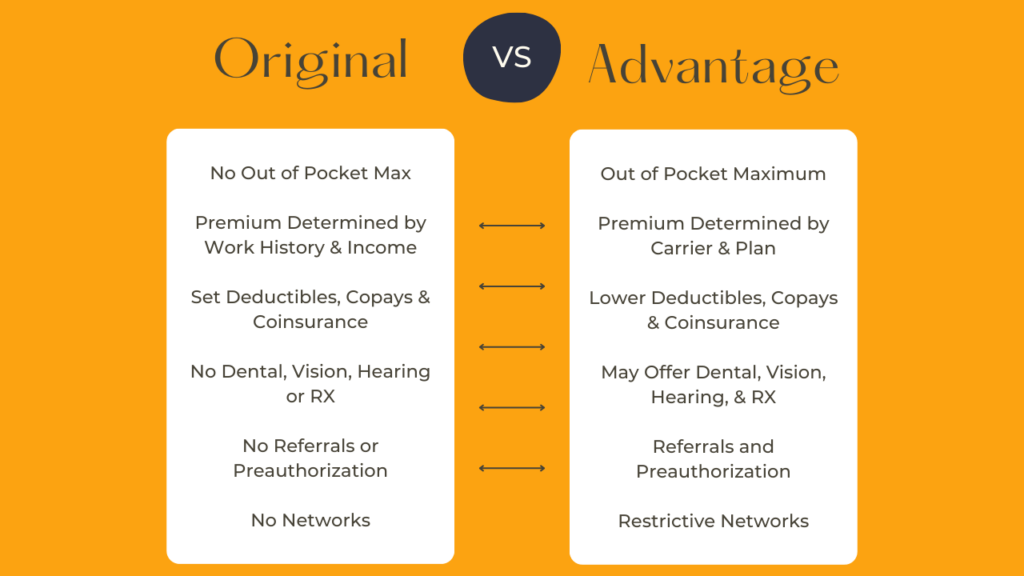

Although Medicare provides comprehensive coverage, there are financial gaps:

- Part A Deductible

- Part B Deductible

- Part A Copays/Coinsurance

- Part B Copays/Coinsurance

Also, there is in out of pocket maximum. To fill in these financial gaps and provide extra protection, we strongly recommend a Medicare Supplement Plan.

You’ll also need to choose between Original Medicare (possibly with Medigap) or a Medicare Advantage Plan. There are pros and cons of each.

And don’t forget to enroll on time!

Part B Late Enrollment Penalty: 10% for each 12 month period you are without coverage

Part D: 1% for each full month you are without coverage (after the first 63 days)

Medigap: Although there are no late penalties, if you try to enroll after the 6 month window after you turn 65 and enroll in Part B you can be charged more or denied (based on medical underwriting).