Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

What is Health Insurance

So what is health insurance and why do you need it? Really let’s talk about the second question. These are the complaints we most often hear:

“Why am I going to pay for something if I never use it?”

Or…

“I pay for something and then I have to pay even more when I use it.”

Yes, that’s the way it works.

You pay for it in case you need it. Most preventative services will be covered often with no copay. It’s just there to assist to prevent bill bills and impost and out of pocket maximum (more on that later) to prevent you from going into medical debt.

If you want a plan with lower coinsurance, copays, or deductibles, you will likely have to pick a plan with a higher monthly premium. It’s far from perfect, but that’s the way it works.

People without health insurance are far less likely to go to the doctor for the little things which can suddenly become very big, very serious and very expensive things requiring the emergency room.

Premiums & Premium Tax Credits

Speaking of premiums, your premiums is what you must pay on a monthly basis to keep your insurance active. Now with a few exceptions, such as Short Term Medical insurance, under the ACA, you cannot be charged more or denied based on a pre-existing condition.

If you opt for a plan on the marketplace you may be eligible for significant discounts via premium tax credits.

Based on your MAGI (modified adjusted gross income) you may be eligible for thousands of dollars in premium tax credits. These are just tax credits paid upfront and reflected in a heavily discounted monthly premium

You will be asked to estimate your MAGI. If you overestimate and end up making less than anticipated, you may end up with a larger tax credit when you file your taxes. If you underestimate and end up making more than anticipated, you may have to pay a portion of your premium tax credits back. So, it is very important to keep your information up to date.

Costs

There are, of course, those additional costs when you actually utilize your insurance.

This is the amount that you have to pay out of pocket before your insurance begins to contribute to the cost share. Usually, basic services like preventative care, vaccines, or even a trip to urgent care will be covered before you have met your deductible. You may still have to pay, but not the full deductible.

Deductible

If you are on a family plan there is an individual deductible and a family deductible. If you meet your individual deductible, you are good to go. All money spent counts toward the family deductible on a family plan. So, even if you haven’t met your individual deductible, if your family has met the family deductible, again, you are good to go.

Copays vs. Coinsurance

Copays are a fixed amount for a specific treatment, service, or product. You could have a $20 copay for the doctor, $50 for a specialist, and $500 for the ER. You could have different copays if these are in or out of network on a PPO (again more on that later)

Coinsurance is a percentage. So if your coinsurance is 20%, you pay 20% of whatever the cost is. You are much more likely to get some surprises with coinsurance because of this.

Out of Pocket Maximum

Then there is the OOP MAX. Your plan will have an OOP MAX for covered in network services. Usually a few thousand dollars or more depending upon the type of plan. If you reach your OOP MAX all covered in network services for the remainder of the year will be covered by your plan with no charge to you. There are individual and family OOP MAX that work the same as the deductibles we just talked about.

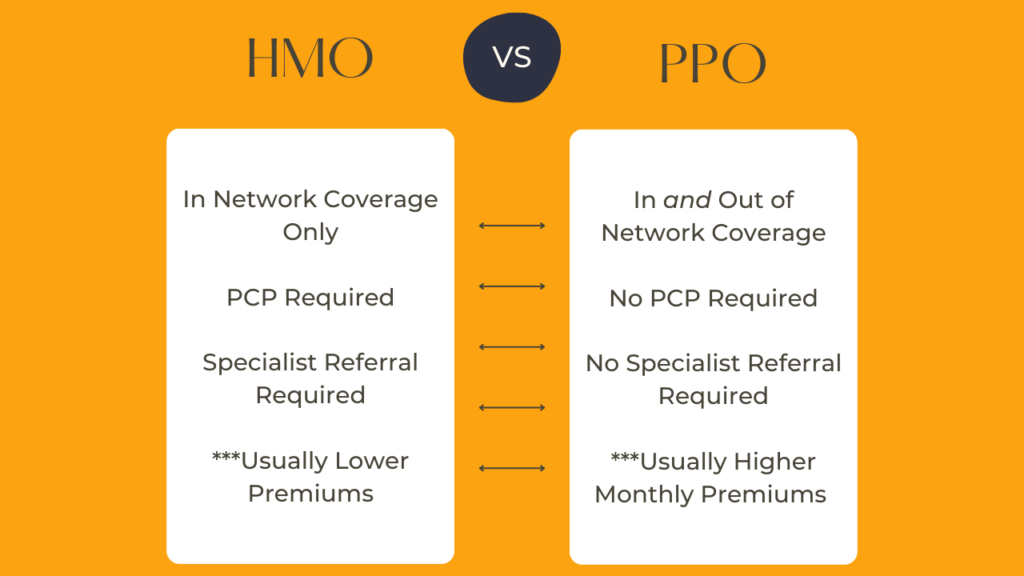

HMO, PPO, EPO

HMO, PPO, and EPO are three different types of plans offered.

HDHP & HSA

More acronyms to throw at you: HSA and HDHP. These are especially popular with the FIRE community or Financial Independent Retire Early.

Will the acronyms never stop???

HDHP stands for high deductible health plan and it is just a type of health plan with a very high deductible. Again for plans on the marketplace, most of those preventative and basic services will likely be covered sometimes with no copay even before you’ve met your deductible.

Usually, these plans will have a lower monthly premium because of the much higher deductible. So, if you are younger or healthier, this can be a good way to save money.

Sometimes these plans offer additional benefits called an HSA or health savings account.

This is a separate account with your money which can be used for qualified medical expenses or as a wealth building tool. As long as it is for a qualified medical expense there is no taxation or penalty. You contribute however much you want (up to the yearly limit as determined by the IRS) and that money is pre-tax- therefore lowering your taxable income. These accounts are interest and that interest is also not taxed. You can invest a certain portion of your HSA and any earnings on those investments are not taxed. This is what’s known as the triple tax advantage.

Hold onto that HSA and the money can roll over from year to year. If you hold onto it until you turn 65, you can convert it to a basic retirement account.

Other Options

There are other options other than the group health insurance offered by your employer or plans offered on the marketplace.

There is private insurance which can be full coverage or short term medical plans. Private insurance will likely have medical underwriting which means preexisting conditions may not be covered or you could be denied. However, for a younger, healthier person, you may have a lower monthly premium. Short term medical plans are now available for a period of up to 3-4 months, but can offer much lower monthly premiums for those ineligible for a premium tax credit. Additionally, private plans will offer more flexibility and the possibility of nationwide PPO coverage.

Catastrophic Coverage Plans through the marketplace are a type of HDHP for those 30 and under. They offer low monthly premiums and high deductibles with up to 3 visits with your PCP before needing to pay your deductible.

Critical Illness Plans and Hospital Indemnity Plans are lump sum payout plans that will offer you a lump sum payout if you need to be hospitalized or are diagnosed with a critical illness based on the terms of your plans. This money is yours to use as you see fit. You can pay medical bills, but you can also pay for groceries or your mortgage. The choice is yours.