Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Looking forward to retirement? Let’s talk about the ways you can make your health insurance work for you.

HSA

If you haven’t yet joined Medicare, let’s start by talking about HSAs or Health Savings Accounts. hey are a type of interest bearing account that may be offered as a benefit with your HDHP.

HSAs offer the triple tax advantage. Contributions are pre-tax, lowering your taxable income. Interest accrued is also not taxed. And as long as you withdraw your funds for qualified medical expenses those funds will not be taxed.

Additionally, you can invest a certain portion of your HSA and the earnings will not be taxed. Hold onto this account until retirement. You can use it as a regular retirement account, but funds will be taxed OR you can use it for those medical expenses we’ve talked about with no taxation.

The IRS sets maximum contributions every year for HSAs and in 2024, that Max is $4150 for an individual or $8300 for a family. But if you are 55 or older you have an additional $1000 you can contribute to “catch up”

Marketplace

If you are not yet of Medicare age and don’t have insurance through your employer, definitely consider a marketplace plan. For those wishing to retire early, these can be a great way to save money!

Marketplace plans offer premium tax credits to those who are eligible based on their income, specifically their MAGI.

If you retire early and are living off of savings then with your reduced income you would likely be eligible for a rather significant premium tax credit.

Part B

Now on the flip side, you may not be retiring early. You may actually be working past the age of 65. If that’s the make sure you go head and defer Medicare Part B.

Follow the instructions on the back of the card and send it back. If you keep the card, you keep Part B and you will be charged for it.

If you are working past the age of 65, make sure to contact Social Security to re-enroll so you are not subject to the Part B late enrollment penalty. At that point, you will likely want to file IRMAA as well.

Prescription Drug Coverage

There are a few prescription drug options that you should be aware of. Our number one recommendation is to enroll in a Part D plan.

Now, some prescriptions may still be very expensive especially if we are talking about specialty medications or tier 5. Because some of these medications can be so expensive, some people feel like Part D just isn’t worth it. However, there are two additional benefits to enrolling in Part D:

Catastrophic Coverage- So if you are someone who has to take some of those more expensive medications, then the catastrophic coverage phase of Part D can help with your medical spending.

Part D has four stages which are basically financial thresholds. These thresholds are set every year by the IRS. In 2024, the catastrophic coverage phase begins at $8000. So if you reach $8000 in prescriptions drug spending, your plan will pay for your prescriptions for the remainder of the year.

Not enrolling in a Part D plan when you are first eligible could make you susceptible to the Part D Late Enrollment Penalty.

Part D Late Enrollment Penalty = 1% of the base beneficiary premium for each month you are without creditable overage (after 63 days(.

So, in all honesty, it’s not a huge penalty (unlike the Part B late enrollment penalty). However, you could certainly avoid it by enrolling in one of the less expensive Part D plans

If you want to put off Part D (or even use in conjunction with Part D) there are pharmaceutical assistance programs and state pharmaceutical assistance programs.

You may notice pharmaceutical assistance programs mentioned at the end of prescription commercials when they say “Financial assistance may be available”.

Some states also offer state pharmaceutical assistance programs.

This is in addition to certain pharmacy coupons as well as things like GoodRX. Compare prices to maximize savings!

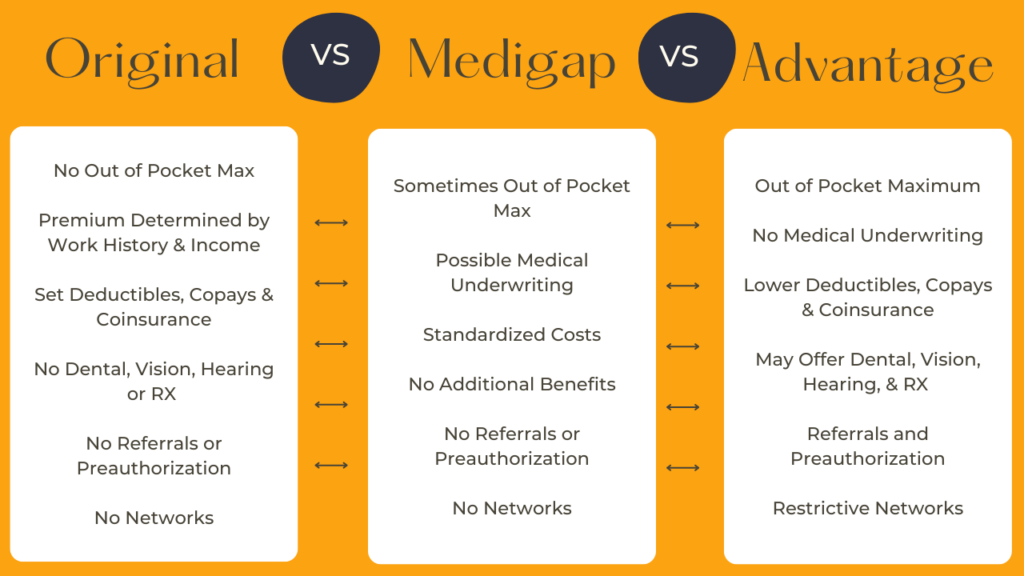

Medigap vs. Medicare Advantage

Health Insurance in retirement is going to cost you money. There is just no way around it. However, you need to put your money to its best use.

There are three main options for Medicare in retirement: