Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Breaking news and huge changes coming to short term medical plans starting Sept. 1, 2024. Read on to learn more so you can enroll before it’s too late!

Changes

As of Sept. 1, 2024, short term medical plans are going to majorly change. In recent years, those interested in a short term medical plan could enroll in a plan for a period of up to three years. As of September 1, you will only be able to enroll for a period of up to 90 days with an option for a one month extension.

Large medical plans are usually able to offer pricing based on the overall health of the group. So, those with larger medical needs are balanced by those with lower medical needs. Since there is no medical underwriting or concerns for preexisting conditions for marketplace plans, this balance works reasonably well.

Short term medical plans can offer lower premiums to those eligible however they require medical underwriting. That means that those that are healthier may opt for a short term medical plan with a lower monthly premium leaving a sicker population to utilize the marketplace plans. This can throw the whole system out of balance.

Also, because the benefits are offered may not be as comprehensive as marketplace plans, sometimes people are left out in the cold when their insurance does not offer the benefits they thought it did.

For example, a man with cancer who was denied coverage because his plan considered it to be a preexisting condition. Or a woman who was left with 20k in medical bills due to an amputation that her carrier would not cover.

That being said for many who are younger and healthier but unable to qualify for a premium tax credit, they may be left with no insurance options. There are many who fall through the cracks making too much for a premium tax credit but still too little to comfortably pay for a full priced plan.

Should we roll back short term medical? Is there a better solution?

Marketplace vs. STM

BUT, there is still time to enroll in a 3 year plan if you’d like. Let’s talk about the pros and cons to help you determine is a short term medical plan is right for you!

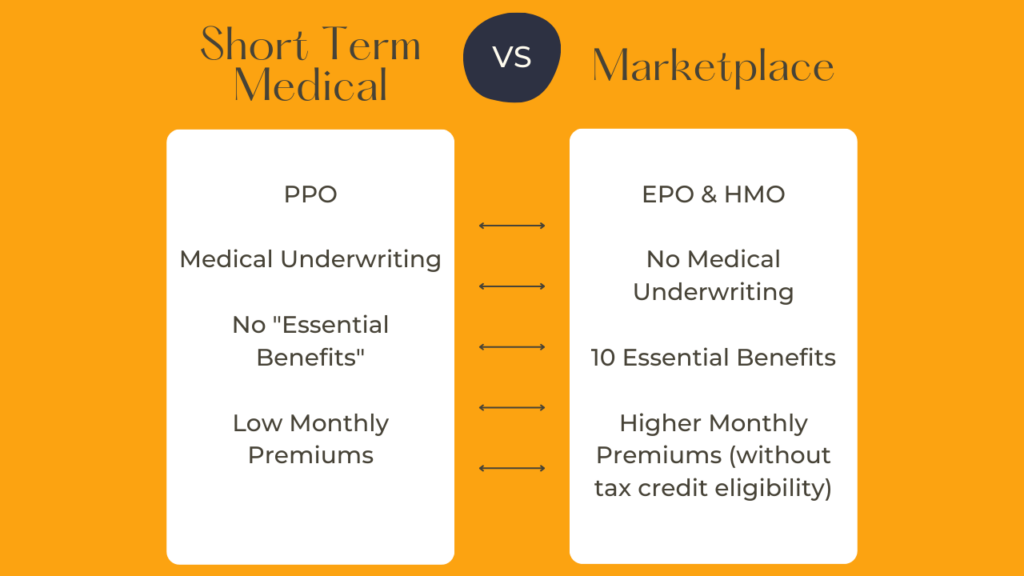

As you can see in the chart, Short Term Medical plans will offer PPOs compared to the EPOs and HMOs of the marketplace. This allows for increase flexibility.

However, STM require medical underwriting which means you could be charged more or denied. Pre-existing conditions may also not be covered.

Additionally, ACA plans offer the 10 Essential Benefits. STM plans do not. Therefore things like pregnancy would not be covered.

However, Short Term Medical plans can offer much lower premiums especially for those who are younger or healthier or don’t qualify for a premium tax credit through the marketplace.