Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Medicare is a guarantee in retirement. Or, is it? Can your Medicare Supplement be denied? What can you do about it?

What is Medigap?

So, first and foremost, what is Medigap? Medigap is a voluntary type of supplemental coverage to fill in the financial gaps of Original Medicare.

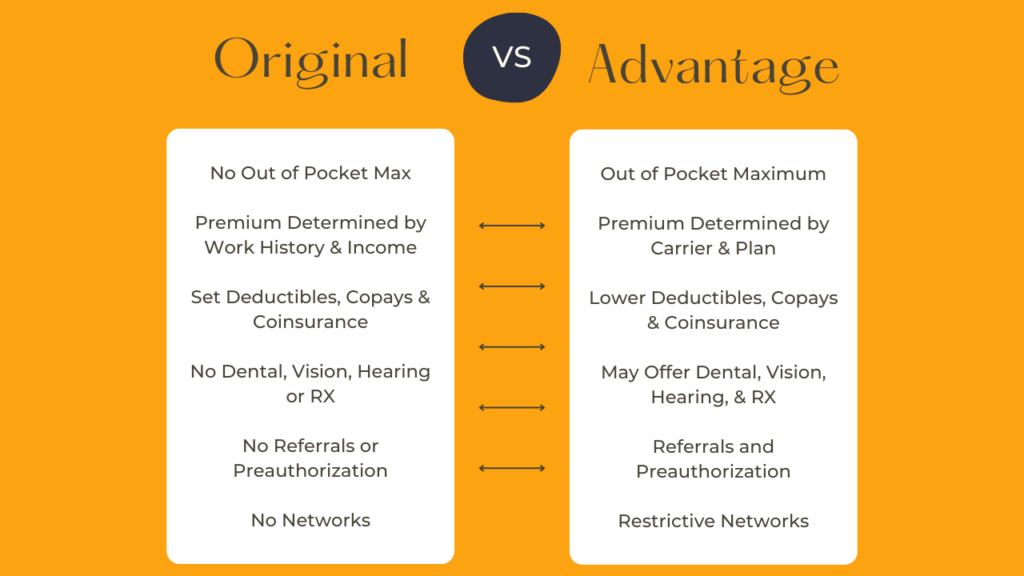

Basically, in addition to the premiums that you have to pay for Original Medicare, there are deductibles and copays or coinsurance. There is also no out of pocket maximum so if you have major medical needs, you could wind up with major medical expenses.

Medigap or Medicare Supplement Plans step in to cover the deductibles and copays/coinsurance. They can also impose an OOP MAX when applicable.

Basically you’ll pay an extra monthly fee to have more of an all-inclusive approach to healthcare with less or possibly no out-of-pocket costs for the year.

Sounds good. So how do you enroll? Can you be denied and what do you do if you are denied?

How/When You Enroll

You can actually enroll in a Medigap plan year round. However, you are best served doing so in the six months after you turn 65 and enroll in Part B. During this time you will not be subject to medical underwriting and therefore you cannot be charged more or denied. So, this is the best time to enroll!

Many people put off enrolling in Medigap when they are first eligible because they are young and healthy and not looking to incur the additional expenses. However, kicking the can further down the line can come back to haunt you. If you choose to enroll at a later date when you are older or with more extensive health needs, you may be subject to medical underwriting and therefore charged more or possibly even denied.

There are some ways that you can enroll past 65 and we will talk about that in just a bit.

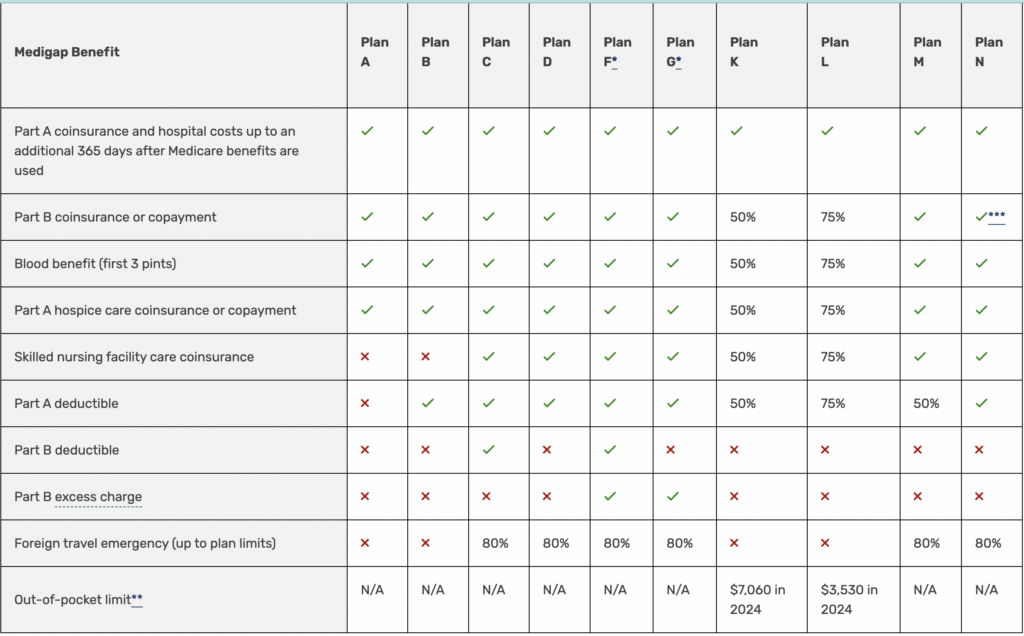

Choosing a Plan

First, you need to decide which plan best serves your needs.

Credit Medicare.gov.

Enrolling after 65

There are times when you can enroll after 65 without medical underwriting.

For example, if you are working past the age of 65 and maintaining creditable coverage through your employer you may have chosen to defer Medicare. If that’s the case, when you retire and lose your coverage at that point you would enroll at Part B. Your 6-month window would begin then.

Another way to enroll past 65 has to do with Medicare Advantage. If you are within the first year or joining a MA plan you are still within your trial right period. You can switch back to Original Medicare at that point and enroll in Medigap.

Also, if you have an MA and you move outside of your network (perhaps to a different state) you can enroll in a Medigap plan instead.

Guaranteed Issue

There are also several states that have at least one enrollment period per year where Medigap is guaranteed issue.

- California

- Connecticut

- Maine

- Maryland

- Massachusetts

- Missouri

- New York

- Oregon

Medicare Advantage

If none of these options are available to you, you can stick with Original Medicare alone (although that can be a little risky with an OOP MAX).

You can also switch to an MA plan. These are an alternative to Original Medicare and there is no medical underwriting. There are pros and cons.