Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

You’ve got your financial retirement plan in place and are ready to hand in your two weeks notice. But what are your health insurance options if you want to retire early?

COBRA

If you’re leaving a job with a group plan then you may be interested in COBRA. This is definitely not our number one recommendation, but you should understand all options available.

COBRA is really only meant as a stop gap between insurance options. However, there are circumstances in which you might want to utilize it and there are pros and cons.

COBRA will allow you to keep your exact same coverage. So, if you have specialized medical needs and see doctors that take limited insurance options, you might want to consider it, at least temporarily.

Unfortunately, COBRA is very cost prohibitive. Under the ACA, employers with at least 50 FTE, must offer affordable health insurance. They pay at least 50% of their monthly premium. With COBRA, you are responsible for your portion and your employer’s portion. Your premium will at least double (possibly more). There may also be a 2% administrative fee.

Obviously COBRA is expensive. However, if you need major medical care and have already met your deductible or even your out of pocket maximum, you may wish to keep it, at least for the time being. Run the numbers to determine your best course of action.

Marketplace

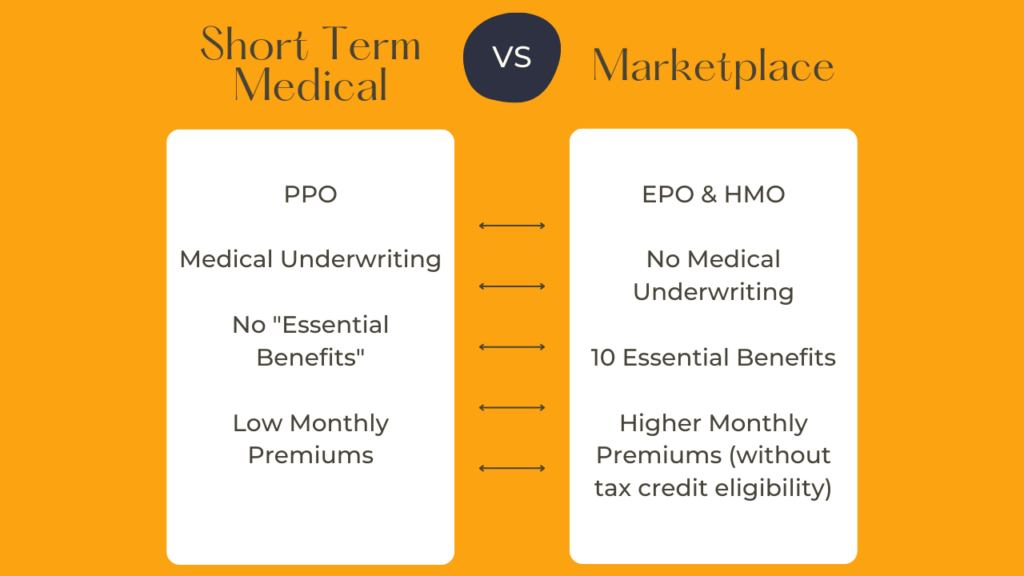

Marketplace plans can be a great option for early retirees. There is no medical underwriting for marketplace plans. When you lose your coverage by leaving your job, you will enter into a special enrollment period.

Marketplace plans must offer at least the 10 essential benefits.Aadditional coverage for vision and dental can be purchased separately.

Eligibility for premium tax credits is determined by your income and household size. So, if you retire early and live largely on savings and assets with a lower income, you will likely be eligible for a rather large premium tax credit which can save you thousands of dollars per year. You may even be eligible for a plan with a $0 monthly premium based on your new post retirement income.

Short Term Medical

If you are not eligible for a premium tax credit of any kind, marketplace plans can be a little pricey. They also can be a little limiting because it is very rare to find PPO plans. If you wish to retire early to travel, a PPO can be especially appealing.

So, if you are ineligible for a premium tax credit, a private insurance plan may be comparable. Let’s talk specifically about short term medical plans.

STM are a type of private insurance. That are renewable for a specified period of time- usually up to three years. There are, of course, pros and cons.

DPC & Catastrophic Coverage (or Critical Illness and Hospital Indemnity)

There are also other creative solutions for health insurance for those who wish to retire early. For example, you could look into Direct Primary Care with some other type of limited health plan.

DPC is not actually health insurance. It’s basically an agreement between you and your doctor in lieu of insurance. Basically, it’s a cash pay option, but done on a monthly basis to cover a variety of services through your PCP.

Now, of course, not all physicians offer this, so you would need to find a PCP that does and it only works for visits to your PCP. So, if you need to see a specialist, take prescription medication or require more extensive medical care, you would be on your own.

For this reason, people who enter into these types of agreements are also encouraged to enroll in a more bare-bones health insurance plan to cover larger medical bills.

Catastrophic Coverage

You could enroll in some type of high deductible health plan such as a catastrophic coverage plan. This won’t really help for minor medical needs but will at least impose an out of pocket maximum to protect you from major medical bills. Usually these plans will have very high deductibles and lower premiums. So, they are inexpensive to maintain. But because they have an out of pocket maximum, if you need to have surgery or care for a large medical concern, you will have have a plan in place to protect your from major medical debt.

Lump Sum Plans

Similarly, you could also compare these types of plan to a critical illness plan which will pay out a lump sum if you are diagnosed with one of several very serious illnesses such as cancer.

You could also choose a hospital indemnity plan which will pay out a lump sum if you need to be hospitalized.

Summary

So, if you want to retire early, in summation:

- Consider COBRA only under certain circumstances.

- Look into Marketplace plans especially if you now have a lower income and are living on savings and assets.

- Consider a STM if you have lower health needs, are ineligible for a premium tax credit or if you really need a PPO (perhaps to travel extensively!)

- Look into some creative combination of DCP with a more bare bones plan to cover your basic needs and cover you in case of larger, unexpected medical needs.