Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Medicare Advantage plans can be very popular as an all inclusive approach to Medicare. But there are definite downsides and many of our clients have encountered absolute nightmares with their Medicare Advantage plans prior to working with us. So let’s discuss the top three Medicare Advantage nightmares and how to avoid them!

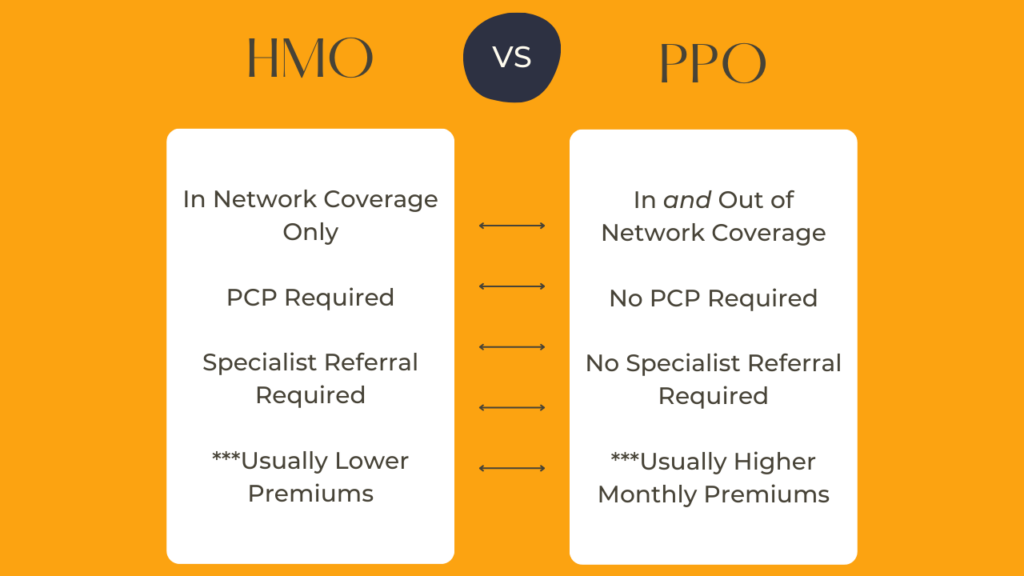

Networks

Medicare Advantage plans are probably more similar to the health insurance that you’ve had in the past because there are networks. If your doctor or hospital is outside of your network then you will likely not have coverage.

This is far more common than you’d expect. Some people report having to travel over an hour to find a doctor who accepts their plan. Although you can usually find a PCP in the network, specialists may be more difficult and if you have a condition that requires a specialist, you certainly don’t want to be limited.

You can avoid this or help to avoid this in one of two ways. Your first option is to enroll in a PPO instead of an HMO.

We also recommend that you check in advance to ensure that the doctors and hospitals you use accept your plan.

Preapproval

Another huge issue with Medicare Advantage plans is preapproval.

MA plans are managed care plans which basically means that not only do you and your doctor have a say in your healthcare, but your insurance carrier does as well. This is an issue with both HMO and PPO plans.

Basically, if your doctor orders a test or treatment your plan may have to pre-approve it before you can even make your appointment.

This can cause a huge delay in receiving necessary treatments or tests or you may be denied and have to pay out of pocket.

Make sure you explain to your doctor that you have a medicare advantage plan and will likely need to submit a letter or documentation from your doctor explaining why this treatment or test is necessary. Call your plan immediately to find out how quick the turnaround time is for pre approvals and see if you can make your appointment before your service has been approved.

Some carriers are better than others with pre-approvals so work with a qualified broker who can guide you towards a better carrier.

Expenses

A lot of nightmare MA situations boil down to one thing: expenses.

If your doctor or hospital is out of network: expenses.

If your treatment or test is denied: expenses.

So, please do your homework in advance.

Additionally, remember to read any bills you receive thoroughly and carefully. Medical billing errors are very common and because MA plans are not as cut and dry and Original Medicare and Medigap, you are much more likely to miss an error.

Some additional expenses come in the form of deductibles, copays and coinsurance and your OOP Max. These vary plan by plan.

You’ll have a deductible to meet. For medical expenses this is usually rather low, but can have a significant cost for hospital expenses. Then of course, there are copays and coinsurances for services, treatments and medications. And then there is an out of pocket maximum to cap your yearly spending.

The problem is that costs like deductibles and out of pocket maximums reset with each plan year. So, if you have significant medical expenses, you’ll have to meet those deductibles and OOP maximums yearly.

These pitfalls can be overcome by sticking with Original Medicare and enrolling in a Medigap plan instead.