Medigap plan K: Overview

Medigap Plan K is one of the standardized Medicare Supplement plans available to beneficiaries seeking additional financial protection beyond what Original Medicare provides. Like all Medigap policies, Plan K is designed to address some of the out-of-pocket costs associated with Medicare Parts A and B, helping to reduce the financial burden of healthcare expenses.

Plan K offers a unique structure compared to other Medigap plans, as it covers a percentage of specific costs rather than providing complete coverage. This approach makes it an appealing choice for individuals looking for supplemental insurance with lower premiums, provided they are comfortable sharing some healthcare costs.

Key Features and Benefits of Medigap Plan K

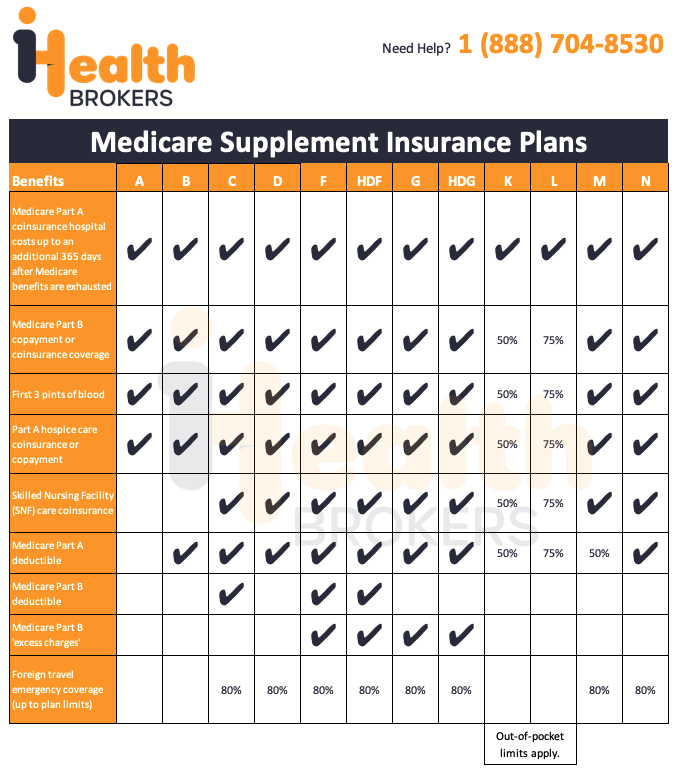

Medigap Plan K is particularly beneficial for covering significant inpatient and skilled nursing care expenses. It provides coverage for 50% of the Medicare Part A deductible, which is the amount beneficiaries are required to pay before Medicare Part A begins to cover hospital expenses. Plan K also covers 50% of coinsurance and copayment costs for Medicare Part A services, including inpatient hospital care and hospice care.

One of the standout benefits of Plan K is its provision for skilled nursing facility care. Following a hospital stay of three days or more, the plan helps cover 50% of the coinsurance costs for skilled nursing care and critical support for individuals requiring extended recovery or rehabilitation. Additionally, Plan K covers 50% of the cost of the first three pints of blood needed for a covered medical procedure, ensuring that beneficiaries are not fully responsible for these expenses.

Despite these advantages, Plan K does have limitations. It does not cover the Medicare Part B deductible or any excess charges that healthcare providers may bill above Medicare-approved amounts. Additionally, it does not provide coverage for medical emergencies occurring during foreign travel, making it less comprehensive than some other Medigap plans, such as Plan G. Beneficiaries should carefully evaluate their healthcare needs and financial situation to determine if Plan K aligns with their priorities.

Enrollment in Medigap Plan K

Enrolling in Medigap Plan K is a straightforward process that begins with meeting eligibility requirements. To qualify, individuals must be enrolled in both Medicare Part A and Part B. The optimal time to enroll is during the Medigap Open Enrollment Period, which begins the month an individual turns 65 and is enrolled in Medicare Part B. These six months grant guaranteed issue rights, ensuring that applicants cannot be denied coverage or charged higher premiums due to pre-existing conditions.

Plan K is offered by private insurance companies, but its benefits are standardized and regulated by the Centers for Medicare and Medicaid Services (CMS). This standardization ensures that the coverage provided under Plan K is consistent across all insurers, allowing beneficiaries to focus on comparing premiums and customer service when selecting a provider.

It is essential for beneficiaries to act promptly during the Open Enrollment Period to secure the best terms for their Medigap coverage. Those who miss this window may face medical underwriting, which could result in higher premiums or denial of coverage based on health status.

Coverage Considerations for Medigap Plan K

While Medigap Plan K provides valuable coverage for many healthcare costs, it requires beneficiaries to share in some of these expenses. This cost-sharing structure is reflected in the 50% coverage for coinsurance and copayments for Medicare Part A and Part B services. Plan K also has an out-of-pocket maximum, which limits the total amount a beneficiary is required to pay in a given year for covered services. Once this maximum is reached, the plan covers 100% of all eligible expenses for the remainder of the year.

However, Plan K does not cover certain expenses that some beneficiaries may find important. For example, it does not provide coverage for the Medicare Part B deductible or excess charges, which occur when a provider charges more than the Medicare-approved amount for a service. Additionally, beneficiaries seeking coverage for medical emergencies while traveling internationally will need to explore other options, as Plan K does not include this benefit.

For those seeking more comprehensive coverage, other Medigap plans, such as Plan G, may be more suitable. Plan G covers the Part B deductible and excess charges, as well as foreign travel emergencies, making it a more extensive option for individuals with higher healthcare needs.

The Value of Medigap Plan K

Medigap Plan K offers a balanced approach to supplemental insurance, combining meaningful cost-sharing with a lower premium structure. This plan is particularly attractive to individuals who are relatively healthy, have predictable medical expenses, or are comfortable with the cost-sharing features of the plan.A

By reducing the financial strain of inpatient care, skilled nursing facility stays, and other essential services, Plan K provides peace of mind and a safety net for unexpected medical needs. However, beneficiaries should carefully consider their specific healthcare requirements, budget constraints, and long-term coverage goals to determine whether Medigap Plan K is the right choice for them.

With its unique blend of cost-sharing and financial protection, Medigap Plan K serves as a valuable option for many Medicare beneficiaries, ensuring that essential healthcare services remain accessible and affordable.

FOOTNOTES:

1. HDF and HDG are deductible versions of the F and G, respectively. If you choose one of these options, this means that you must pay for Medicare-covered costs up to the deductible amount of $2,490 (2022) before your Medigap plan pays anything.

2. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 copayment for emergency room visits that don’t result in an inpatient admission.

3. Plan F, High Deductible Plan F (HDF) & Plan C are ONLY available to those who were considered Medicare-eligible prior to 2020.

4. Out-of-pocket limits for Plan K are $6,620 (2022) and $3,310 (2022).