Medigap plan G: Overview

Medigap Plan G is a supplemental insurance policy designed to help Medicare beneficiaries manage out-of-pocket healthcare expenses. This plan provides additional coverage for costs that Original Medicare does not fully address, such as deductibles, coinsurance, and co-payments. By bridging these gaps, Medigap Plan G ensures greater financial predictability for enrollees, particularly those with significant healthcare needs.

To qualify for Medigap Plan G, individuals must already be enrolled in Medicare Parts A and B. The plan complements these primary Medicare components by covering certain expenses for Part B services, which include outpatient care, preventive services, and doctor visits. However, it is important to note that Medigap Plan G does not include prescription drug coverage, as those benefits are provided under Medicare Part D. Furthermore, like all Medigap policies, Plan G does not cover every expense excluded by Medicare. Beneficiaries may still encounter out-of-pocket costs depending on the nature of their medical care.

Despite its limitations, Medigap Plan G is widely regarded as a valuable addition to a Medicare enrollee’s healthcare coverage. It provides robust protection against unforeseen medical expenses and reduces the financial strain associated with coinsurance and deductibles.

Why Medigap Plan G is Popular

Medigap Plan G is among the most sought-after supplemental Medicare plans. This popularity stems from its extensive coverage and relatively affordable premiums compared to other comprehensive Medigap options. Plan G covers virtually all of Medicare’s deductibles, including those for inpatient hospital stays under Part A. It also addresses the coinsurance and co-payments for Medicare Part B services, alleviating the financial burden for routine and unexpected medical care.

For many enrollees, the primary appeal of Medigap Plan G lies in its balance of cost and coverage. While it does not cover the Medicare Part B deductible, the policy offers significant savings in other areas, making it a practical choice for individuals with moderate to high medical expenses. Its comprehensive nature ensures that beneficiaries are protected from many of the unpredictable costs associated with healthcare, allowing them to budget with greater confidence.

Enrollment in Medigap Plan G

Enrolling in Medigap Plan G is a straightforward process facilitated through private insurance companies authorized to offer Medigap policies. Individuals can begin by researching the plans available in their area and comparing the offerings from different insurers. Premiums and coverage options may vary slightly between providers, so careful evaluation is critical to finding a plan that meets individual needs and budget constraints.

State Departments of Insurance are excellent resources for beneficiaries seeking guidance on Medigap Plan G enrollment. These departments can provide information about licensed insurers and ensure that beneficiaries work with reputable providers.

Enrollment is most advantageous during the Medigap Open Enrollment Period, which begins the month an individual turns 65 and is enrolled in Medicare Part B. During this six-month period, applicants have guaranteed issue rights, meaning they cannot be denied coverage or charged higher premiums due to pre-existing health conditions. After this period, eligibility may depend on medical underwriting, and individuals could face higher costs or restrictions based on their health history.

The Value of Medigap Plan G

Medigap Plan G represents an essential investment in financial security and peace of mind. By covering substantial out-of-pocket expenses, this plan helps individuals avoid the financial hardships that can accompany serious illness or chronic medical conditions.

Though it does not cover prescription drugs, dental care, or vision services, Medigap Plan G pairs well with other Medicare options, such as Part D for drug coverage or standalone policies for dental and vision care. Together, these plans create a comprehensive healthcare strategy tailored to the specific needs of the enrollee.

In conclusion, Medigap Plan G stands out as a popular and practical choice for individuals seeking to enhance their Medicare coverage. Its ability to cover nearly all Medicare deductibles, coinsurance, and co-payments—combined with relatively manageable premiums—makes it an attractive option for those looking to minimize their out-of-pocket healthcare expenses. By carefully evaluating their options and understanding their healthcare needs, beneficiaries can use Medigap Plan G to achieve a more secure and predictable healthcare experience.

FOOTNOTES:

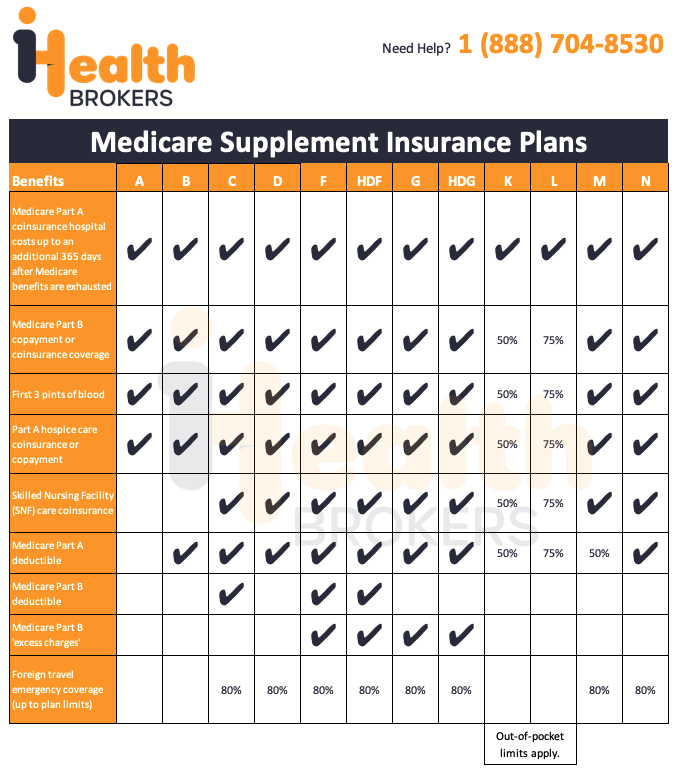

1. HDF and HDG are deductible versions of the F and G, respectively. If you choose one of these options, this means that you must pay for Medicare-covered costs up to the deductible amount of $2,490 (2022) before your Medigap plan pays anything.

2. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 copayment for emergency room visits that don’t result in an inpatient admission.

3. Plan F, High Deductible Plan F (HDF) & Plan C are ONLY available to those who were considered Medicare-eligible prior to 2020.

4. Out-of-pocket limits for Plan K are $6,620 (2022) and $3,310 (2022).