Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Medicare Advantage and Medicare Supplement plans are two different solutions to address some of the gaps in Original Medicare.

But that is where the similarities end.

Unfortunately, Medicare is complicated. And very often these differences are not entirely clear to Medicare Beneficiaries. Consequentially, people often sign up for a Medicare Advantage Plan because they are more widely marketed and with what is often a higher commission, they are sometimes pushed a little bit more than Medigap plans. Additionally, Medicare Advantage plans offer many enticing benefits not offered by Medigap.

The problem is that once you have enrolled in Medicare Advantage, it is not always so easy to make the switch back to Original Medicare and add a Medicare Supplement Plan.

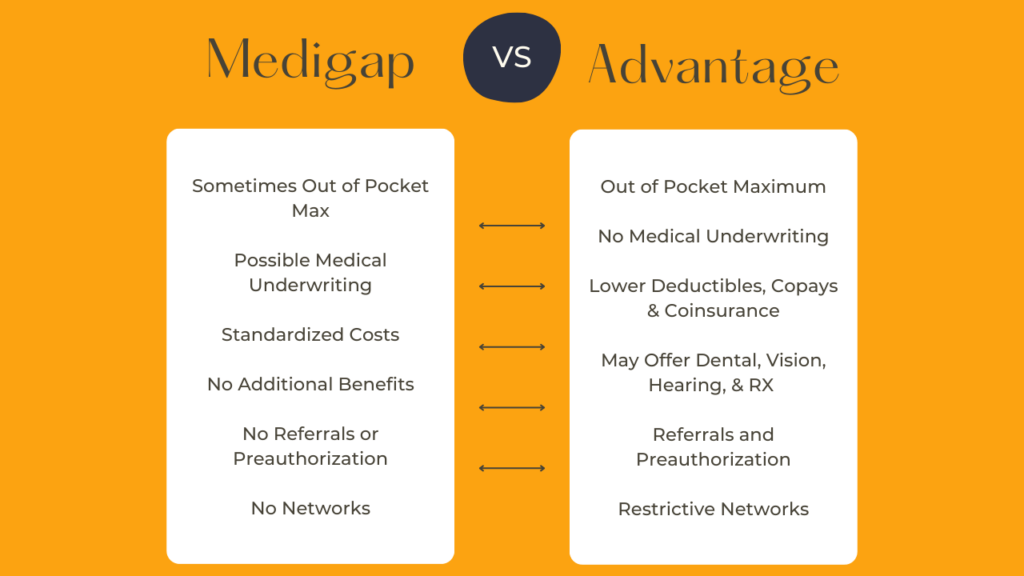

Medigap vs. Medicare Advantage

So Original Medicare offers truly comprehensive coverage. But there are out of pocket costs such as deductibles and copays or coinsurance. There is also no OOP MAX.

Additionally, as you’ve noticed Original Medicare does not offer some much needed benefits such as dental, vision, hearing, or prescription drugs.

To address these concerns, many people look to MA or Medigap.

Costs

In an ideal world, we would almost always recommend Medigap over MA. With Medigap, you have the ultimate flexibility, no networks, no referrals, no preauthorization. These are major drawbacks with MA. However, how do the costs compare?

Unfortunately, it is not that simple.

Looking at premiums alone, Medicare Advantage plans will almost always seem to be less expensive. However, with Medicare Advantage plans you run the risk of having to go out of network or even being denied for services or treatments.

Often times, if you are healthy and only making basic use of your health insurance, a Medicare Advantage Plan will save you money. However, as you age and need to make more regular use of your health insurance or your need to actually treat diseases or conditions, a Medicare Supplement plan will likely be more cost effective.