Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Your Medicare agent or broker is supposed to work for you. They are supposed to be on your side and serve as your liaison, so it’s imperative that you work with someone whom you can trust.

And while most Medicare agents are honorable, like with anything, there can be some that are less than scrupulous in their actions. That is why it is of the utmost importance that you are informed and aware of any red flags you should be on the lookout for.

How are Medicare Agents Paid?

Medicare agents and brokers are paid on commission. Different types of plans offer different commissions. That is not to say that steering you towards a higher commission plan is a bad thing.

For example, Plan G might offer a larger commission. But Plan G is, in all honesty, one of the best supplement plans available to new enrollees. It offers the most comprehensive coverage and will cover almost all of your out of pocket expenses.

Because of this, Plan G tends to be one of the more expensive plans. So, it is far more likely that your agent is steering you towards this plan because it is simply one of the best.

If you need something with Plan G level coverage, you should also compare costs to Plan N and even discuss the HDHP version of Plan G. A good agent or broker will be happy to compare and contrast these plans and discuss the pros and cons of each plan offered.

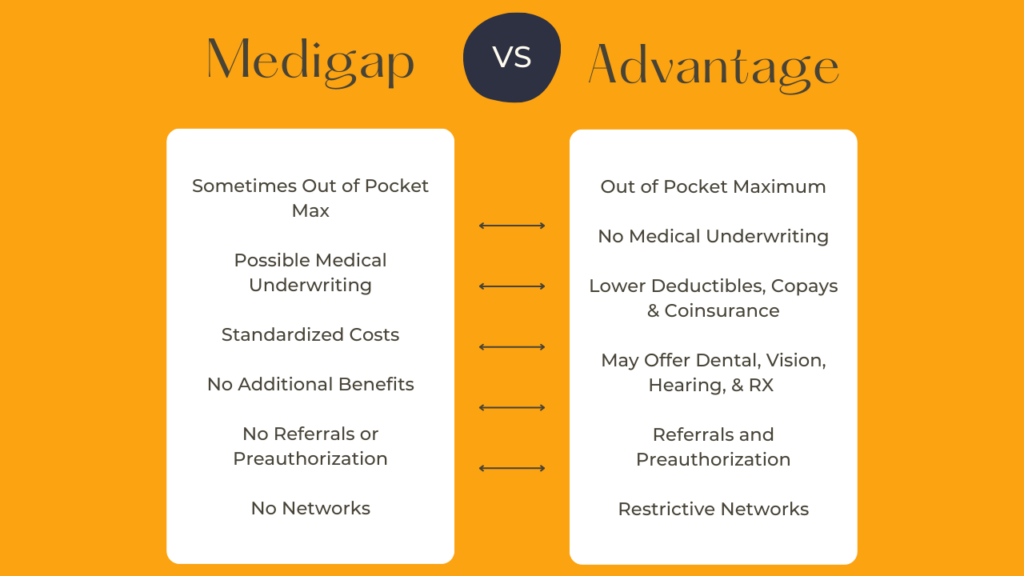

Medicare Advantage

Medicare Advantage has a less than stellar reputation, however, over half of Medicare Beneficiaries are enrolled in one.

MA plans are marketed much more heavily and they do pay higher commissions. But that doesn’t mean that all Medicare Advantage Plans are bad or that you shouldn’t consider ones. There are pros and cons

MA plans may not be a great option if you have extensive health needs. A Medicare Supplement plan would be far better in those cases. But you cannot just switch to a Medigap plan at any time in most states.

However, if you live in a state with more flexible medigap enrollment (or if you live in Florida, where MA plans are just much better), an agent or broker might suggest that you enroll in an MA plan to save money until your medical needs become more extensive.

A good agent should thoroughly discuss the pros and cons of an MA plan with you and also discuss the enrollment process for a Medigap plan in case you need to switch down the line. They should also discuss the hospitals and healthcare networks in your area to make sure that you will not have issues finding medical care.

Like with Plan G, just because MA plans offer higher commission, that may not be the only reason that your agent recommends one. Many MA are just much cheaper than Medigap plans, and if you are living on a fixed income, you may not be able to afford the higher Medigap monthly premiums.

In an ideal world, we’d likely recommend a higher coverage Medigap plan, but that may just not be financially feasible.

There are also other situations where Medicare Advantage plans may be helpful to you. For example, if you qualify for Medicaid in addition to Medicare, a DSNP, which is a dual eligibility special needs plan (a type of MA plan) may offer your excellent coverage.

Just like with anything else, if you feel pressure and you don’t feel your agent or broker is taking the time to discuss your needs thoroughly, this is a red flag.

Agent vs. Broker

An agent is a representative of the carrier-meaning they work for the health insurance company, not you. They can only discuss plans offered by their company.

A broker works for you, not the carrier. They can discuss all of the different plans and companies that they can offer. That’s not to say that an agent isn’t trying their best or working to serve your needs, they just may be more limited in their offerings.

Part D

Original Medicare does not cover prescription drugs. For that, you will need a Part D Plan. Part D plans can be very inexpensive and often offer agents and brokers small commissions. As a result, some agents and brokers cannot be bothered.

Big red flag.

Your agent or broker should be there to help you. If our clients have issues or questions about their plans, even after they have enrolled, we are there to help. We don’t get paid for those phone calls, and a good agent or broker should be willing to assist with these types of issues.

Medigap

It is unlikely that an agent or broker would steer you towards Medigap if it’s not in your best interest for multiple reasons:

- Medigap often just IS the better option.

- Agents and brokers will usually make less commission on Medigap plus Part D, vs Medicare Advantage.

However, Medigap plans can be easier. Benefits are standardized, and once you enroll, it can be very difficult to switch. So, it is likely that you will just re-enroll every year.

That being said, if you ever feel rushed or pressured, that is a red flag.