Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Can your doctor deny your Medicare coverage? Yes and no, let’s talk about it.

Medicare Parts

Although it is very unlikely that your doctor would deny Original Medicare, there are several parts to Medicare and that’s where things can get confusing.

- Part A

- Part B

- Part C

- Part D

- Medigap

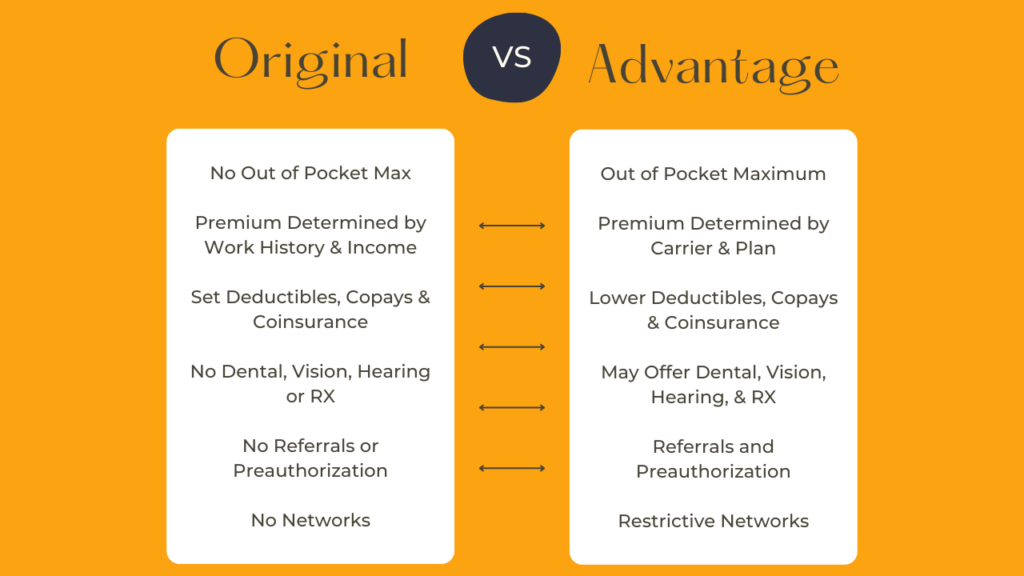

Original Medicare

Part A and Part B comprise Original Medicare. Truthfully it is highly unlikely that a doctor or hospital would deny your Original Medicare coverage. Original Medicare doesn’t have a network because it is not offered by private carriers. It’s estimated that somewhere around 97% of doctors accept Original Medicare.

So maybe it’s not that your doctor doesn’t accept Original Medicare. Maybe it’s that the specific service isn’t covered. Medicare doesn’t cover:

- Long-term care

- Dental care

- Eye exams (for prescription glasses)

- Dentures

- Cosmetic surgery

- Massage therapy

- Hearing aids and exams

Medigap

Now what about Medigap? Medigap is also known as Medicare Supplement Plans. They fill in the financial gaps of Original Medicare but do not offer additional benefits.

Medigap plans can help to cover:

- Part A Coinsurance

- Part B Coinsurance

- First 3 Pints of Blood for Transfusion

- Par A Hospice Care Coinsurance/Copay

- Skilled Nursing Facility Care Coinsurance/Copay

- Part A Deductible

- Part B Deductible

- Part B Excess Charges

- Foreign Travel Emergency

These types of plans are offered by private carriers. So, does that mean your doctor might not accept your plan if they aren’t in the network for the carrier?

Actually, no!

If your doctor accepts Original Medicare, they accept your Medicare Supplement Plan regardless of who your carrier is

So, you can pretty much shop your plan based solely on price. Because plan benefits also remain the same regardless of who your carrier is.

But a warning!

Prices do tend to increase on a yearly basis so you want to go with a carrier with a history of low, stable increases as opposed to erratic or dramatic increases. Remember, after your initial 6-month window, you may be subject to medical underwriting for a Medigap plan which means you could be charged more or denied. So, it’s not usually very easy to switch plans on a yearly basis. A broker can help you with these histories.

Part D

Let’s jump past Part D because these are really prescription drug plans. So, your doctor isn’t really going to accept them or not accept them because they don’t have much to do with doctors. That being said, make sure that your prescriptions are included in your Part D formulary to ensure you have coverage.

Medicare Advantage

And now onto the main event: Medicare Advantage aka Medicare Part C. These are managed care plans that are offered by private carriers. They are a replacement for or alternative to Original Medicare. And this is where things can get a little dicey!

Unlike Medigap plans, your career with Medicare Advantage plans matters! And many doctors do not like to contract with Medicare Advantage Plans.

If you are still going to go the Medicare Advantage route, you may want to go with a PPO to provide more flexibility.