Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

This Medicare Advantage plan will offer you all the same benefits as Original Medicare plus dental, vision, hearing, prescription drugs, exercise benefits and more. And you don’t have to pay anything extra for it?

Sound familiar?

This is a common pitch for Medicare Advantage. And all of these things are very often true! But there are downsides that obviously aren’t advertised as frequently.

There are many options parts of Medicare, one of which is a Medicare Supplement Plan.

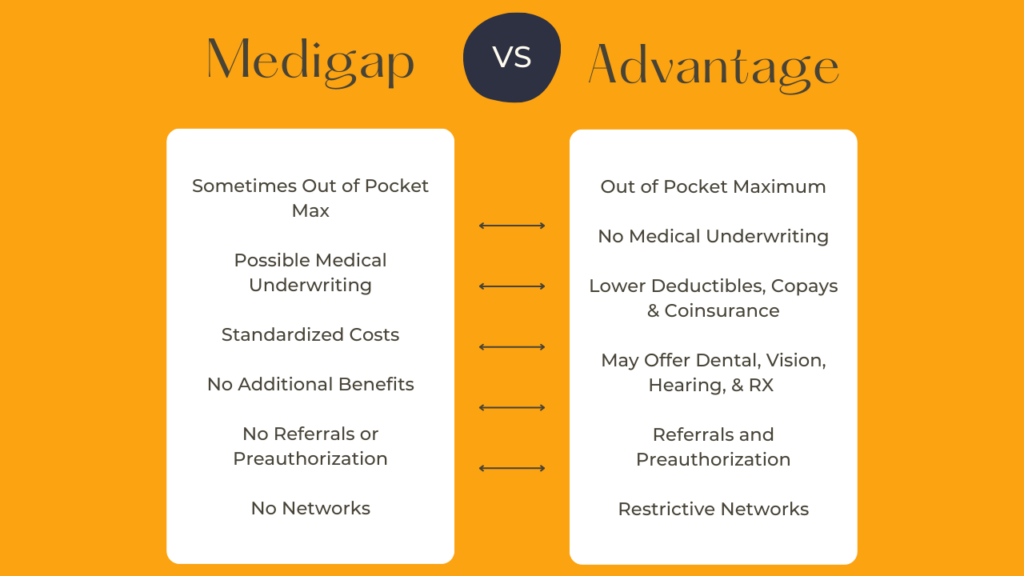

Medigap

So, why and when would you choose a Medigap Plan vs. a Medicare Advantage Plan?

Let’s start with Medigap. Medigap will fill in the financial gaps of Original Medicare. Because it’s not offering additional benefits, it is really just a financial solution to the out of pocket costs associated with Original Medicare. Regardless of who your carrier is, if your doctor accepts Original Medicare, they will accept your Supplement plan.

This will give you tremendous flexibility because there are no networks. You can really take charge of your own health because in addition to network, there are no referrals.

Original Medicare offers excellent coverage, but there are costs that Medigap plans can step in to cover. These costs include deductibles and copays/coinsurance. Depending upon your health and frequency of care, you could have thousands of dollars in bills. And, there is no out of pocket maximum with Original Medicare alone.

Of course, if you remain in the pinnacle of health, it is unlikely you will have large costs with Original Medicare. That being said, realistically speaking, at some point or another, you will deal with some type of medical crisis. At that point, having supplemental coverage is rather crucial.

If you are diagnosed with a serious medical condition, you could easily surpass 60 days of coinsurance within a given benefits period and wind up having to pay those very high daily rates. Remember, you could be released and readmitted within the same benefit period and that would count towards those 60 days.

If you need to recover in an SNF, you could very easily surpass those 20 days that are covered at no charge. It’s difficult to find hard numbers, but many studies indicate that SNF stays averaged between 20-30 days. Those daily copays are significant.

That’s not even taking into consideration lifetime reserve days or the possibility of more than one benefit period and therefore more than one hospital deductible in a given year.

If you can afford some type of Medigap plan, we highly encourage you to enroll.

There are 10 different plans to choose from. Regardless of who the carrier is, because these plans are offered by private carriers, benefits will remain the same. So it is much easier to shop for these plans. First determine which type of plan suits your needs (Plan G, Plan N, etc…) Then find a carrier with the best price.

Medigap Enrollment

You can actually enroll in a Medigap plan year round. There is no specific yearly enrollment period (Except in a few states).

However, it is in your best interest to do so in the six months after you turn 65 and enroll in Part B. During this time you will not be subject to medical underwriting. That means you cannot be charged more or denied based on your health. Should you choose to enroll outside of this 6 month window, you may be subject to medical underwriting which means you could be charged more or denied.

And this is much more common than you may think. Often people are pretty healthy when they first retire and don’t want the extra expense of a Medigap plan.

However, if you wait until your health declines and you are more in need of a Medigap plan, at that point it is very likely that your plan options will be very limited or possibly non-existent.

Medicare Advantage

MA plans are much more similar to the types of insurance you’ve had in the past. So, there will be networks and benefits and costs will vary widely. Because of that, they are much harder to shop.

The two biggest disadvantages of Medicare Advantage are networks and preauthorization.

Medicare Advantage plans operate on networks which means you can choose between HMOs or PPOs. Obviously PPOs will give you much more flexibility, but many beneficiaries describe extreme difficulty in finding someone who accepts their plan.

An even bigger problem is preauthorization. MA plans are managed care plans. That means that between you, your doctor, and your care stands your insurance carrier. If your doctor recommends a certain service or treatment, your insurance carrier must first approve it. That means a lot of paperwork, followup phone calls and hoops to jump through. It can also mean frightening big bills and added stress during what can already be a very stressful time.

However, there are many benefits offered by Medicare Advantage plans. For example, many plans offer additional benefits such as:

- Dental

- Vision

- Hearing

- Prescription Drugs

An added benefits of MA is that unlike Medigap, there is of course, no medical underwriting. As far as enrollment you can either enroll when you first become eligible or during the AEP.