Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Medicare is confusing! Let’s go over some tips and tricks to help you master your Medicare!

Know When to Enroll

You’ll first become eligible for Medicare when you turn 65. Most people are automatically enrolled. If you don’t receive your medicare card in the mail, you’ll need to contact social security. You need to do so in the 7 month window surrounding your 65th birthday (three months before, the month of and three months after).

If you are maintaining creditable coverage through your employer by working past the age of 65, please go ahead and defer Part B by following the instructions and sending the card back. There is a monthly premium for Part B and if you receive insurance through your employer, you won’t need the extra coverage.

When you do retire and lose your coverage, make sure to re-enroll or you may be subject the Part B Late Enrollment Penalty.

You will have to pay 10% of your Part B premium for each 12 month period you are without creditable coverage. This penalty will be tacked onto you monthly premium forever!

Other Enrollment Periods

There are other enrollment periods as well for Medicare Advantage, Part D and Medigap.

Your first opportunity to enroll in Medicare Advantage or Part D is that same 7 month window. There is also the AEP or annual enrollment period.

Every year from October 15-December 7th you can sign up for or switch your Part D or MA plan. Part D is for prescription drugs to be used in conjunction with Original Medicare. MA is a replacement for Original Medicare- more on that in just a bit.

Bonus tip for MA. There is also the MAOEP which is Jan.1-March 31. During this time you can drop your MA plan or switch plans, you just can’t sign up for MA. Also, if you are within your first year of signing up for Medicare Advantage, you are within your trial right period and you can drop and switch back to Original Medicare at any time.

Finally, there is Medigap. These work to fill in the financial gaps of Original Medicare. More on that, later in the video.

You can technically apply for a Medigap plan at any time. However, it is in your best interest to do so in the 6 month window after you turn 65 and enroll in Part B. During this time you will not be subject to medical underwriting.

After this 6 month window, you may be subject to medical underwriting which means you could be charged more or denied. There are some states however that have guaranteed issue or that have yearly enrollment periods guaranteed issue.

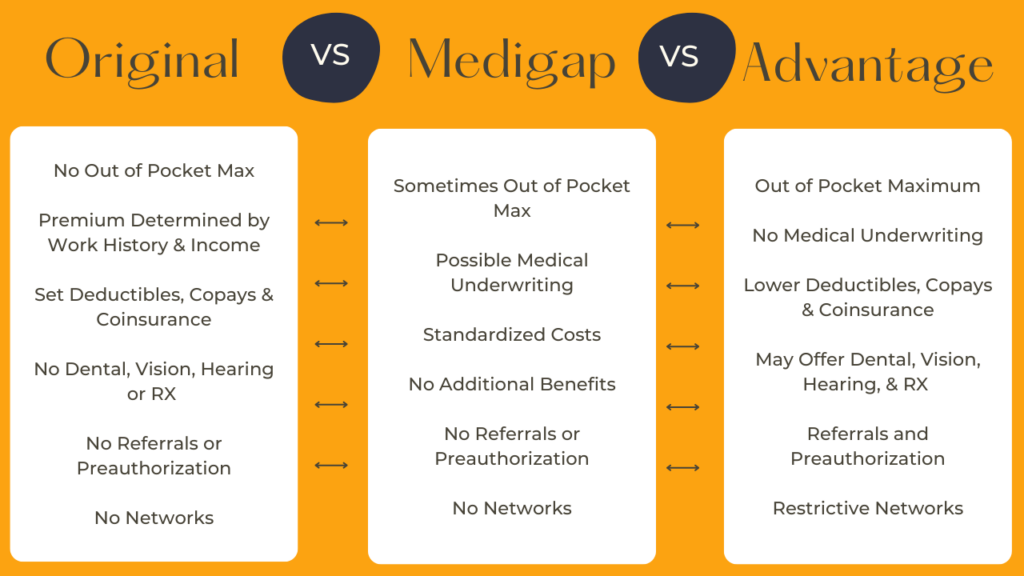

Original Medicare or MA

One of the biggest things you need to understand in order to master your Medicare is the difference between Original Medicare and Medicare Advantage.

Which Medigap Plan

Now let’s talk about Medigap. These are extremely popular because they are basically the all inclusive approach to healthcare. You’ll pay a little more upfront in the form of an additional monthly premium, but will have most, if not all, of your out of pocket expenses covered.

There are 10 plans to choose from:

IRMAA

Finally, let’s talk about IRMAA. Did you know that you might actually be paying too much for Part B? Your Part B premium is tied to your income, but Medicare is looking at income from two year’s prior. If you are making less money (perhaps because you have retired), you may be paying too much for Medicare!