Jesse Smedley

Jesse Smedley is the Principal Broker for iHealthBrokers and the founder, president, and CEO of Smedley Insurance Group, Inc. and iHealthBrokers.com. Since the inception of SIG in 2007, Jesse has been dedicated to helping people save money on their health insurance by providing them with resources to educate themselves on all their health insurance options, both under age 65 and Medicare beneficiaries. He is featured in many publications as well as writes regularly for expert columns regarding health insurance and Medicare.

Many individuals believe they are covered, but hidden gaps in their plans can leave them vulnerable to high medical costs. Have you ever stopped to think about what would happen if you were involved in a serious accident or were diagnosed with a chronic illness? The thought of it is terrifying, and the financial burden can be crippling.

One of the most significant challenges people face is understanding the nuances of their health insurance plans, and it’s not uncommon for individuals to find themselves underinsured. Even if you have health insurance, it’s crucial to understand what your plan covers and what it doesn’t. After all, having health insurance is only half the battle – you need to make sure it’s providing adequate coverage. So, let’s dive into some of the potential pitfalls that might be hiding in your plan.

When was the last time you reviewed your health insurance policy? If you’re like most people, it’s probably been a while. But it’s essential to regularly review your coverage to ensure it’s still meeting your needs. One of the biggest mistakes people make is assuming that their health insurance plan will cover everything. Unfortunately, that’s not always the case. There are often hidden gaps in coverage that can leave you financially exposed. For instance, what happens if you need a specific medication or treatment that’s not covered by your plan? These unexpected expenses can add up quickly, leaving you with a hefty bill.

We’ve all heard the horror stories about people getting stuck with massive medical bills, even when they have health insurance. It’s a frightening reality, and it’s more common than you might think. The truth is, health insurance companies often have strict guidelines about what they will and won’t cover. And sometimes, even if you have health insurance, you might still be left with significant out-of-pocket expenses. So, how can you protect yourself from these unexpected costs? That’s what we’re going to explore in this video.

Let’s face it – health insurance can be confusing. There are so many terms and concepts to understand, from deductibles to copays, and it’s easy to get overwhelmed. But understanding these concepts is critical to ensuring you have adequate coverage. So, buckle up, and let’s break down some of the key components of health insurance.

OOP Costs

Sometimes benefits are covered but with a significant cost. Or perhaps they are covered, but not yet.

Deductibles, copayments, and out-of-pocket maximums – these are some of the most critical aspects of health insurance, and they can significantly impact your financial security during a health crisis. A deductible is the amount you need to pay out of pocket before your insurance kicks in. Copayments, on the other hand, are the fixed amounts you pay for specific services, like doctor visits or prescription medications. Then there’s the out-of-pocket maximum, which is the total amount you’ll pay for healthcare expenses in a year. These elements can make or break your financial stability during a medical emergency.

When it comes to health insurance, knowledge is power. Understanding how deductibles, copayments, and out-of-pocket maximums work can help you make informed decisions about your coverage. For instance, if you have a high deductible, you might need to pay more upfront costs before your insurance covers the rest. But if you have a low deductible, your premiums might be higher. It’s all about finding that delicate balance between affordable premiums and adequate coverage.

The way you approach health insurance depends on your individual circumstances. If you’re someone who rarely gets sick, you might opt for a lower premium and a higher deductible. But if you have ongoing health issues, you might need a plan with more comprehensive coverage. The key is to understand your health needs and choose a plan that aligns with them.

10 Essential Benefits

Under the ACA, all plans must offer at least the 10 essential benefits. This applies to group health insurance plans through your employer as well. Private insurance and short term medical plans may of course be exempt from these regulations.

But what you should be aware of is the extent of these benefits and any stipulations that may surround them.

For example, mammograms are of course covered, but you may only be able to get one under 40 with a referral from your doctor.

There are many preventative services and screenings that are offered with no charge even if you haven’t met your deductible,but if the service becomes diagnostic rather than preventative, you may be charged.

For example, colorectal cancer screenings, colonoscopies are covered and considered preventative care.

But if your doctor finds a polyp or anything that needs to be tested, it becomes diagnostic and could therefore have a charge associated.

Prescriptions

Prescriptions will be covered as one of the ten essential benefits. But is your prescription covered?

Well you need to check your plan’s formulary. A prescription drug might be covered, but if your doctor has prescribed it for off label purposes, it might not be. You may be able to work around this with preauthorization from your insurance carrier. Your doctor will likely need to submit paperwork indicating why this specific medication is necessary.

You could also be denied if you try to refill too early or too frequently, based on certain types of medications.

Sometimes the pharmacy may be out of network.

If you run into issues, talk to your doctor about alternative medications, especially generics, to save money. You can also look into discount programs like GoodRX or state pharmaceutical assistance programs.

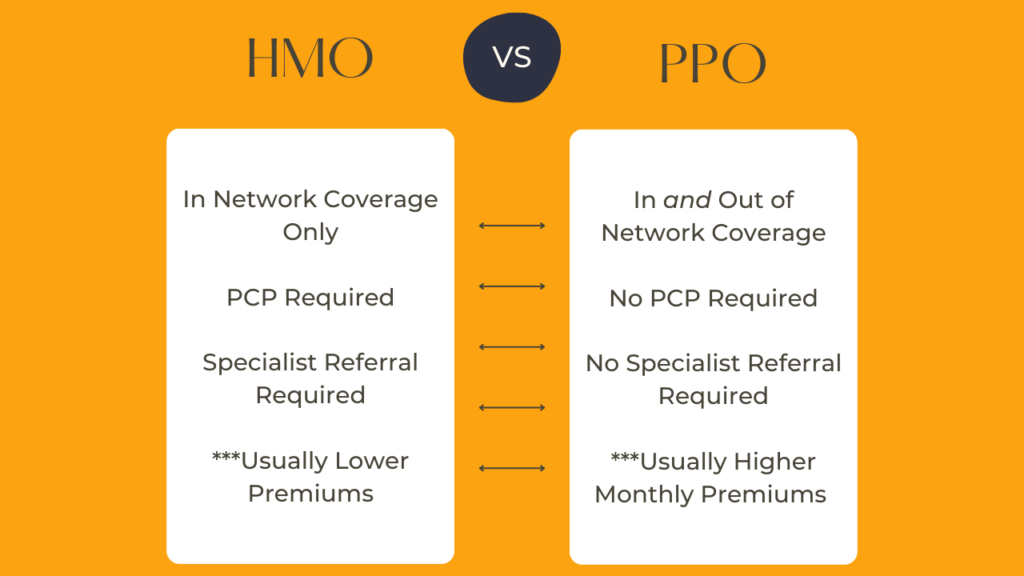

Networks

Do you have an HMO, PPO, or EPO? Depending on your answer, you may have coverage or not.

The moment of truth: Are you really covered? It’s time to strip away the misconceptions and get real about health insurance. One of the most significant misconceptions is that having health insurance means you’re fully protected. But that’s not always the case. Even with health insurance, you might still face surprise medical bills or uncovered expenses. Another misconception is that you can’t afford to change your health insurance plan. However, not having adequate coverage can end up costing you more in the long run.

It’s essential to evaluate your health insurance plan regularly to ensure it’s meeting your changing health needs. Don’t assume that your current plan will always be sufficient. Life is unpredictable, and your health needs may change over time. By understanding the components of health insurance, you can make informed decisions about your coverage.

Health insurance is not a one-size-fits-all solution. What works for someone else might not work for you. That’s why it’s crucial to take an active role in understanding your health insurance plan. Don’t be afraid to ask questions or seek guidance from a professional. And most importantly, don’t wait until it’s too late.

To wrap up, we’ve explored the critical components of health insurance and emphasized the importance of reviewing your coverage regularly to avoid being underinsured. Remember, having health insurance is just the first step – it’s up to you to ensure you have adequate protection.